Request Consultation

Request ConsultationThe global buy now pay later market is set to surge to USD 9.22 trillion by 2032 with a CAGR of 29% during the forecast period 2023 to 2032. In 2021, North America dominated the market, accounting for over 30% of worldwide sales.

The global buy now pay later market size accounted for USD 753.53 billion in 2022 and it is expected to reach around USD 9,226.65 billion by 2032.

According to a survey conducted in July 2020, approximately 56% of Americans have used a buy now pay later service, up from 38% the year before. Consumers have a high affinity and involvement with this type of point-of-sale installment loan, which leads to large recurrent usage. More experienced consumer groups use these financing solutions 15 to 20 times per year and go onto these applications ten to fifteen times per month to browse or shop. While the average credit score of those who use these services is below 700, this is due to thin credit files rather than a lack of credit history. In Asia and Latin America, card-linked installments are the most common method of point-of-sale financing. In contrast, U.S. card issuers, such as American Express Plan It and Citi Flex Pay, have developed post-purchase installment features, but adoption rates have remained low. In the U.S., these post-purchase payments are unable to compete with the 0% annual percentage rate options available at the time of purchase.

Fintechs like SplitIt, network-offered resolutions in trial stages like Visa payments, and cobranded or barely targeted merchant mergers like Chase and Citi's with Amazon are all currently offering card-linked instalments at purchase in the U.S. The average ticket size is roughly $1,000, and bigger credit bands have a higher adoption rate. In the future years, card-linked instalments will be a table-stakes skill, but those that can integrate it across the buying experience and efficiently monetize prepurchase services are likely to stand out.

According to the research study, 40% of buy now pay later customers in the U.S. have missed more than one payment, and 72% have seen their credit score drop. As laws differ by state, it's difficult to fit buy now pay later within U.S. legislation. Consumer credit regimes are regulated by federal and state laws, depending on the varying definitions of credit covered by those laws. As now-buy-later providers do not originate loans to clients, the country's lending regulations cannot be fully applied to them because they facilitate and support installment plans on behalf of the customer. According to the latest data, retail purchases utilizing buy now pay later increased fourfold in the U.S., from $24 billion in 2020 to $100 billion in 2021. Globally, the e-commerce market is worth trillions of dollars, with amazing year-over-year growth potential.

Several companies are competing for market share in the U.S. As a result, buy now pay later companies are pursuing mergers and acquisitions in order to accelerate growth and expand into new areas around the world. In August 2021, Affirm formed a strategic partnership with Amazon in the U.S. to let online shoppers to use the buy now pay later payment method to complete transactions of $50 or more. The relationship with Affirm is notable because it is Amazon's first strategic partnership in the U.S. In addition, Square declared the acquisition of Afterpay in August 2021 in order to penetrate one of the fastest-growing consumer payment marketplaces. Square, for example, paid a total of $29 billion for Afterpay. This acquisition is expected to aid Square in quickening its expansion in the U.S. while also allowing it to keep up with PayPal, which has grown into a big player in the worldwide buy now pay later industry.

Many pre-existing financial concerns, such as missed payments and dwindling credit limits, were compounded by the COVID-19 pandemic. Because of this, total credit card usage in the U.S. has decreased in recent years, allowing for the emergence of new payment options, which buy now pay later took advantage of. Buy now pay later solutions were created as an alternative to credit cards and other types of financing, allowing customers to buy a product and pay for it over time in a predetermined number of instalments. Customers are frequently provided these solutions with low to no interest rates and no hidden costs, implying that there is no additional expense to the customer. The market for buy now pay later lending in the U.S. was worth a few billion dollars in 2019, but it is expected to rise by 1,200% by 2024.

Growing adoption ‘buy now pay later’ by consumers

A 'during purchase' payment option is buy now pay later. It ensures that customers enjoy the best shopping experience possible by providing them with quick credit at the point of purchase. Some providers can accept you in under a minute. When compared to traditional credit providers and high-street banks, buy now pay later is a clear winner for customers. Buynowpaylater solutions are based on highly customized and targeted technology that allows customers to connect with platforms without friction. Klarna, for example, offers a QR code that customers may scan to make a payment. Other providers use the capability of the Unified Payments Interface to make purchasing transactions as simple as possible.

The buy now pay later concept is around providing consumers with credit and allowing them to pay later, either in one lump sum or in instalments. This allows customers to shop even if they don't have any cash on hand. In addition, instalment payments aid financial organization by spreading out consumption over a longer period of time. Fees and interest are usually waived on buy now pay later credit. This option is suitable as long as you do not default on a payment. The commissions they charge merchants are how many of these suppliers make money. Lay Buy, for example, charges firms a 4.75%charge while indicting customers nothing. As fintech don't often conduct hard credit searches, consumers with poor credit ratings can benefit from buy now pay later payment facilitation. They typically run soft searches that have no bearing on your credit score.

Consumers have benefited from a wide range of benefits as a result of their use of buy now pay later. To begin with, its ease of use meant that purchases made with the payment method could be done without any friction during checkout, resulting in a simple shopping experience. The ability to defer payments and spread the cost is buy now pay later platform’s key unique selling proposition, making it easier on consumers' wallets, especially those whose income has slowed due to the epidemic. Furthermore, the payment plans given are often interest-free, ensuring that customers are not overcharged while using this credit option to pay for the service or goods they are purchasing.With buy now pay later growing more popular as a payment method, shops should consider adding the service to their checkout. According to ECOMMPAY, nearly three-quarters (71%) of customers would abandon their shopping cart if their chosen way of payment was not accessible. The buy now pay later model, like all financial plans, can become more demanding and unfavorable if applied wrongly.

Rising number of e-commerce platforms

Buy now pay later, by which individuals seek alternative methods of financing, which has been aggravated by the coronavirus pandemic, solutions that allow consumers to pay in interest-free instalments are growing in favor. And, as the market grows, so does rivalry among financial services firms.The coronavirus epidemic has boosted the expansion of the ecommerce business, raising demand for simple online financing choices. The rise in ecommerce enhanced the reach of buy now pay later suppliers because their products are native to online buying. Millions of people were laid off as a result of the pandemic, and they needed more purchasing freedom. However, many people paid off debt during the financial crisis, making interest-free buy now pay later solutions a more appealing option than piling up another huge credit card amount.

Layaway and instalment payments have been modified in the buy now pay later industry to provide consumers with more flexible payment alternatives for their purchases. Buy now pay later solutions, unlike credit cards, are applied to individual transactions, making them acceptable to consumers who want to make a smaller financial commitment, even on lower-ticket items. Because of the pandemic's influence and buy now pay later platform's overall appeal, the industry will generate $680 billion in transaction volume by 2025. This implies a 13.23% compound annual growth rate (CAGR) from the $285 billion the industry was expected to generate in 2018.While some buy now pay later solutions are available in-store, they are more commonly available while purchasing online because they are native to ecommerce checkout. With ecommerce sales expected to grow by 44.4% year over year (YoY) in Q2 2020, more consumers may opt to use buy now pay later solutions on a more frequent basis, if they haven't already.

Electronics – 71%, fashion and lifestyle accessories – 67%, and everyday shopping items – 57% are the most popular buy now pay later purchases. Low or no interest rates, flexibility and ease, and non-eligibility for credit cards are all factors that influence the buy now pay later platform's decision. The number of people who use the buy now pay later is catching up to those who use credit cards. Nearly half of the respondents say they pay with both buy now pay later and credit cards, and 45% say they prefer to pay with buy now pay later even if they have a credit card.

Growing strategic initiatives by key market players

The buy now pay later market has a moderately fragmented. Both customers and merchants benefit from buy now pay later. Expanding their presence and capturing new consumers, prominent suppliers are making their way into the e-commerce sector. By 2025, the market for these buy now pay later payment apps is likely to expand 10-15 times, according to Bank of America Corporation. Customers are increasingly using buy now pay later to make in-store and online transactions. A large number of shops are emphasizing the acceptance of these point-of-sale and online instalment loans as payment methods, providing potential for buy now pay later solution providers to expand. During the projected period, the market is expected to be driven by the expanding e-commerce industry.

Consumers are beginning their journeys within the Pay in 4 providers' apps rather than utilizing Pay in 4 at merchant checkouts, since the top providers are converting into shopping applications. In February 2021, for example, about 17% of Afterpay's customers began one or more transactions from within their shopping app. 7 Consumers can use the Pay in 4 options when shopping from within the app, even if the merchant does not have this capability incorporated at checkout. Customers who shop through the Klarna app, for example, can use Klarna at Amazon, despite the fact that Klarna is not available at Amazon's checkout.

Off-card financing companies like Affirm and Uplift, for example, typically finance midsize purchases between $250 and $3,000 in monthly instalments. The average ticket costs around $800, and the loans are typically for eight to nine months. Electronics, furniture and home products, sports and home exercise equipment, and travel are some of the most popular verticals. Unlike Pay in 4 solutions, which are completely subsidized by the merchant, off-card financing models have originations where customers pay an annual percentage rate, which is sometimes partially subsidized by the merchant, for example, in lower-margin verticals like travel.

The number of big participants in the buy now pay later platform sector are introducing improved and new solutions to fulfill the ever-changing demands of diverse enterprises. A large number of shops are emphasizing the acceptance of these point-of-sale and online installment loans as a payment mechanism, providing potential for buy-now pay-later solution providers to expand. PayPal Holdings, Inc., for example, said in September 2021 that it had agreed to purchase Paidy, a major two-sided payments platform and supplier of buy now, pay later solutions in Japan. The collaboration will broaden PayPal's competencies, distribution, and significance in Japan's domestic payments sector, which is the world's third largest e-commerce market, while also complementing the corporation'scurrent cross-border e-commerce operation there.

Future prospects for ‘buy now pay later

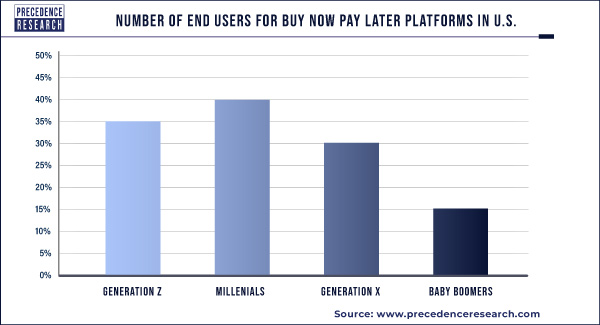

Generation Z and younger Millennials, having grown up as a result of the 2008 financial crisis and graduated into tight job markets, are more cautious about spending, debt, and hidden fees than earlier generations. They have new needs for financial services as digitally informed consumers. They demand simplicity and ease of use, as well as devices that seamlessly interface with other applications they utilize. Traditional banking services are unappealing to this new generation of customers because of their high interest rates, stringent restrictions, and complicated lingo. As a result, leading buy now pay later service providers like Klarna and Afterpay, with their accessible approach to personal finances, bright branding, and creative collaborations with lifestyle companies, focus exclusively on this consumer category.Buy now pay later programs generally provide the same benefits as credit cards, but without the commitment or interest payments. Users can use the services right away, without having to go through any application or background checks. They can also defer payments for longer periods of time than monthly credit card billing cycles, giving them more flexibility in cash flow management.

Buy now pay later services are poised to further disrupt the traditional banking sector as the most recent wave within the greater fintech industry. Because of the Covid-19's long-term financial impact, especially among younger generations, buy now pay later programs are anticipated to gain traction in the future. With established competitors such as PayPal entering the fray, the market will become increasingly crowded, with major banks, fintech start-ups, and tech behemoths vying for consumer attention and market dominance.Meanwhile buy now pay later approach has primarily been employed in retail and e-commerce, it can be used in a variety of different industries. As a result, buy now pay later services are likely to expand to other industries, such as groceries and physical stores, paving the path for new omnichannel applications. As the market grows, buy now pay later applications may evolve into more comprehensive platforms that allow users to gain insight into their spending habits, receive personalized budgeting advice, and find new products based on previous purchases.Furthermore, due to variances in living expenses and income cycles among nations, buy now pay later services may be tailored to meet the demands of different economies. While the buy now pay later model may appear to be just another payment mechanism in industrialized economies, it has the ability to change the game in underdeveloped countries by bringing unbanked people into the mainstream economy.

View Full Report@ https://www.precedenceresearch.com/buy-now-pay-later-market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com | +1 650 460 3308

About the Authors

Aditi Shivarkar

Aditi, Vice President at Precedence Research, brings over 15 years of expertise at the intersection of technology, innovation, and strategic market intelligence. A visionary leader, she excels in transforming complex data into actionable insights that empower businesses to thrive in dynamic markets. Her leadership combines analytical precision with forward-thinking strategy, driving measurable growth, competitive advantage, and lasting impact across industries.

Aman Singh

Aman Singh with over 13 years of progressive expertise at the intersection of technology, innovation, and strategic market intelligence, Aman Singh stands as a leading authority in global research and consulting. Renowned for his ability to decode complex technological transformations, he provides forward-looking insights that drive strategic decision-making. At Precedence Research, Aman leads a global team of analysts, fostering a culture of research excellence, analytical precision, and visionary thinking.

Piyush Pawar

Piyush Pawar brings over a decade of experience as Senior Manager, Sales & Business Growth, acting as the essential liaison between clients and our research authors. He translates sophisticated insights into practical strategies, ensuring client objectives are met with precision. Piyush’s expertise in market dynamics, relationship management, and strategic execution enables organizations to leverage intelligence effectively, achieving operational excellence, innovation, and sustained growth.