North America Spirits Market Size is USD 261.11 Billion in 2026

North America Spirits Market (By Product: Whiskey, Vodka, Gin, Rum, Brandy, Other; By Distribution Channel: Liquor Stores, On-trade, Online, Other; By Caps & Closure: Screw-top, Bar-top / Cork, Other; By Caps & Closure Material: Metal, Plastic, Other) Industry Size, Share, Growth, Trends 2026 to 2035.

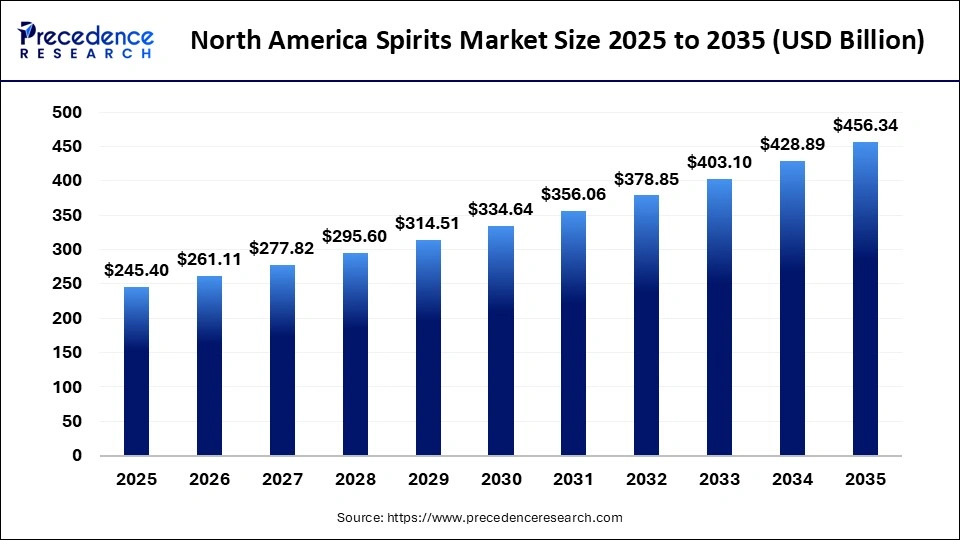

The North America spirits market size was estimated at USD 245.4 billion in 2025 and is predicted to increase from USD 261.11 billion in 2026 to approximately USD 456.34 billion by 2035, expanding at A CAGR of 6.40% from 2026 to 2035. Growing demand for premium and craft spirits is driving the expansion.

North America Spirits Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 245.4 Billion |

| Market Size in 2026 | USD 261.11 Billion |

| Market Size by 2035 | USD 456.34 Billion |

| CAGR 2026 to 2035 | 6.40% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The North American spirits market stands as one of the most mature yet dynamically evolving sectors within the global alcoholic beverage industry. Encompassing a diverse array of distilled beverages, including whiskey, vodka, gin, rum, brandy, and other specialty liquors, the market thrives on a combination of tradition and innovation. With a rich heritage rooted in centuries of distillation practices, particularly in the United States and Canada, spirits possess deep cultural and economic significance within the region.

Evolving consumer preferences, characterized by a rising demand for craft cocktails, flavored spirits, and low-alcohol options, are significantly influencing market trends. Health-conscious consumers are favoring low-calorie, antioxidant-rich, and lower-alcohol products. The increased value consumers place on experiential consumption is contributing to the growth of bars, tasting events, and home bars, thereby enhancing the North American spirits industry.

Moreover, digital influences, convenience, and ethical considerations are critical determinants of today's U.S. spirits consumer behavior. Online communities, social media, and e-commerce platforms are integral to discovery and purchasing decisions, highlighting the necessity for robust digital engagement by brands. The surge in popularity of ready-to-drink cocktails underscores a strong demand for convenience without sacrificing quality or sophisticated flavors, catering to the evolving habits of at-home consumption and on-the-go lifestyles.

The spirits market is benefiting from the growing adoption of technology, initiatives aimed at enhancing operational efficiency, and the expansion of infrastructure development in key economies. The rising demand for scalable and high-performance solutions is further boosting adoption rates within this sector.

North America Spirits Market Share, By Product, 2025 (%)

| Segments | Shares (%) |

| Whiskey | 28% |

| Vodka | 25% |

| Gin | 15% |

| Rum | 10% |

| Brandy | 8% |

| Other | 14% |

- Whiskey - Strong consumer preference and premiumization trends, with a 28% share, establish whiskey as the leading product segment.

- Vodka - Wide consumption and versatility in cocktails, with a 25% share, support demand but remain below whiskey dominance.

- Gin - Growing craft and premium appeal, with a 15% share, contributes but does not lead the market.

- Rum - Steady demand in mixed drinks and regional markets, with a 10% share, supports the market but remains limited.

- Brandy - Niche consumption and traditional preference, with a 8% share, restrict broader dominance.

- Other - Diverse alcoholic beverages, with a 14% share, contribute significantly but do not surpass whiskey.

North America Spirits Market Share, By Distribution Channel, 2025 (%)

| Segments | Shares (%) |

| Liquor Stores | 40% |

| On-trade | 35% |

| Online | 15% |

| Other | 10% |

- Liquor Stores - Wide availability and strong consumer preference for in-store purchases, with a 40% share, establish liquor stores as the leading distribution channel.

- On-trade - Strong presence in bars and restaurants, with a 35% share, supports demand but remains below liquor stores.

- Online - Growing digital adoption, with a 15% share, contributes but does not surpass traditional channels.

- Other - Miscellaneous distribution channels, with a 10% share, result in a smaller contribution.

North America Spirits Market Share, By Caps & Closure, 2025 (%)

| Segments | Shares (%) |

| Screw-top | 50% |

| Bar-top / Cork | 40% |

| Other | 10% |

- Screw-top - Convenience, cost-effectiveness, and widespread usage, with a 50% share, establish screw-top closures as the leading type.

- Bar-top / Cork - Premium appeal and traditional usage, with a 40% share, support demand but remain below screw-top dominance.

- Others - Limited use of alternative closure types, with a 10% share, restrict overall market contribution.

North America Spirits Market Share, By Caps & Closure Material, 2025 (%)

| Segments | Shares (%) |

| Metal | 60% |

| Plastic | 30% |

| Other | 10% |

- Metal - Durability and compatibility with various closure types, with a 60% share, establish metal as the leading material segment.

- Plastic - Cost-effective and lightweight properties, with a 30% share, support demand but remain below metal dominance.

- Others - Alternative materials, with a 10% share, contribute moderately but do not lead the market.

Top CompaniesNorth America Spirits Market

- Diageo Plc

- Pernod Ricard

- Constellation Brands, Inc.

- Asahi Group Holdings, Ltd

- Rémy Cointreau

- Brown-Forman

- Bacardi Limited

- Suntory Holdings Limited

- Davide Campari-Milano N.V.

- William Grant & Sons

Segments Covered in the Report

By Product

- Whiskey

- Vodka

- Gin

- Rum

- Brandy

- Other

By Distribution Channel

- Liquor Stores

- On-trade

- Online

- Other

By Caps & Closure (Type)

- Screw-top

- Bar-top / Cork

- Others

By Caps & Closure Material

- Metal

- Plastic

- Others

| Product | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Whiskey | 0.28 | 0.29 | 0.29 | 0.30 | 0.30 | 0.31 | 0.31 | 0.32 | 0.32 | 0.33 | 0.33 |

| Vodka | 0.25 | 0.26 | 0.26 | 0.27 | 0.27 | 0.28 | 0.28 | 0.29 | 0.29 | 0.30 | 0.30 |

| Gin | 0.15 | 0.16 | 0.16 | 0.17 | 0.17 | 0.18 | 0.18 | 0.19 | 0.19 | 0.20 | 0.20 |

| Rum | 0.10 | 0.11 | 0.11 | 0.12 | 0.12 | 0.13 | 0.13 | 0.14 | 0.14 | 0.15 | 0.15 |

| Brandy | 0.08 | 0.09 | 0.09 | 0.10 | 0.10 | 0.11 | 0.11 | 0.12 | 0.12 | 0.13 | 0.13 |

| Other | 0.14 | 0.15 | 0.15 | 0.16 | 0.16 | 0.17 | 0.17 | 0.18 | 0.18 | 0.19 | 0.19 |

| Distribution Channel | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| On-trade | 0.40 | 0.41 | 0.41 | 0.42 | 0.42 | 0.43 | 0.43 | 0.44 | 0.44 | 0.45 | 0.45 |

| Liquor Stores | 0.35 | 0.36 | 0.36 | 0.37 | 0.37 | 0.38 | 0.38 | 0.39 | 0.39 | 0.40 | 0.40 |

| Online | 0.15 | 0.16 | 0.16 | 0.17 | 0.17 | 0.18 | 0.18 | 0.19 | 0.19 | 0.20 | 0.20 |

| Other | 0.10 | 0.11 | 0.11 | 0.12 | 0.12 | 0.13 | 0.13 | 0.14 | 0.14 | 0.15 | 0.15 |

Research Methodology

Related Databooks

March 2026

April 2026

April 2026

April 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting