U.S. Plastics Market Size is USD 99.45 Billion in 2026

U.S. Plastics Market (By Product: Polyethylene (PE), Polypropylene (PP), Polyurethane (PU), and Polyvinyl Chloride (PVC); By End-use: Packaging, Building & Construction, Electrical & Electronics, and Automotive; By Application: Injection Molding, Blow Molding, Roto Molding, and Compression Molding) Industry Size, Share, Growth, Trends 2026 to 2035.

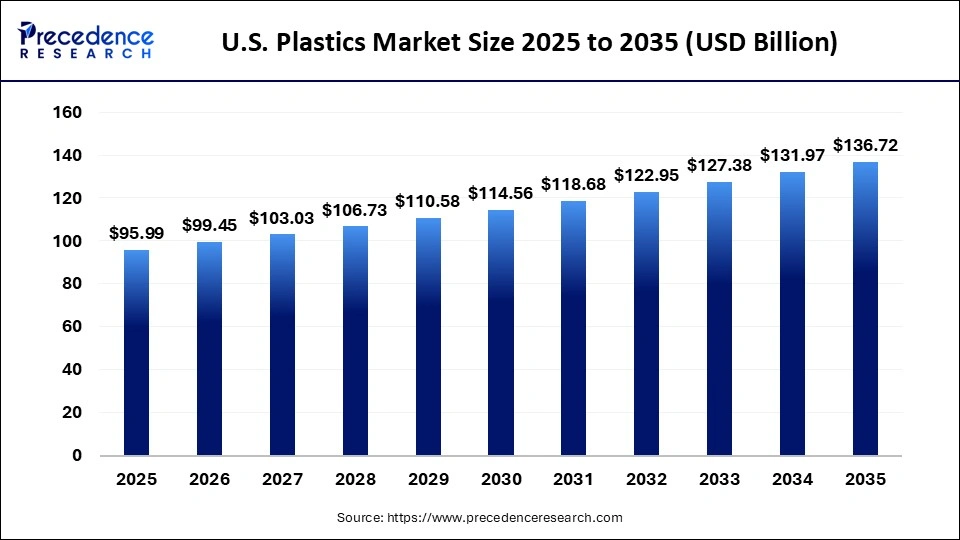

The U.S. plastics market size was estimated at USD 95.99 billion in 2025 and is predicted to increase from USD 99.45 billion in 2026 to approximately USD 136.72 billion by 2035, expanding at A CAGR of 3.6% from 2026 to 2035. The market is largely influenced by increasing demand within the packaging, automotive, and construction industries, coupled with a growing shift toward sustainable materials and initiatives supporting a circular economy.

North America Polyurethane Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 95.99 Billion |

| Market Size in 2026 | USD 99.45 Billion |

| Market Size by 2035 | USD 136.72 Billion |

| CAGR 2026 to 2035 | 3.6% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The U.S. plastics industry plays a significant role in driving economic activity, particularly within packaging, automotive, construction, and healthcare sectors. Its affordability, durability, and versatility have contributed to the gradual replacement of traditional materials such as metal and wood. Additionally, the industry supports manufacturing competitiveness through a substantial trade surplus in resin, serving as a major export contributor to nations such as Mexico and Canada.

The market is evolving to prioritize sustainable solutions, such as chemical recycling, circular plastics, and biodegradable materials, fostering the development of future green infrastructure. Plastic remains a critical component in construction applications like pipes, insulation, and durable materials, aligning with U.S. government efforts to enhance infrastructure. Prominent companies driving growth in this sector include Dow Inc., ExxonMobil Chemical, and LyondellBasell Industries.

U.S. Plastics Market, By Product, 2025 (%)

| Segments | Shares (%) |

| Polyethylene (PE) | 24% |

| Polypropylene (PP) | 35% |

| Polyurethane (PU) | 14% |

| Polyvinyl Chloride (PVC) | 27% |

- Polyethylene (PE) - Polyethylene (PE) represents a dominant segment, holding 24% shares, in the U.S. plastics market, valued for its versatility, cost efficiency, and strong demand across major industries such as packaging, construction, and consumer goods.

- Polypropylene (PP) - Polypropylene (PP) plays an important role in the market, holding 35% shares, characterized by its versatility, low density, and durability, which make it integral to applications like packaging, automotive lightweighting, and medical devices.

- Polyurethane (PU) - Polyurethane (PU), holding 14% shares, plays a significant role in the market due to its versatility, performance, and capacity to meet essential industrial requirements such as energy efficiency and weight reduction, particularly in the construction and automotive industries.

- Polyvinyl Chloride (PVC) - Polyvinyl Chloride (PVC), holding 27% shares, is a key component of the market as the third-most produced synthetic plastic polymer globally, known for its adaptability, affordability, and widespread application in building, construction, and healthcare sectors.

U.S. Plastics Market, By End-Use, 2025 (%)

| Segments | Shares (%) |

| Packaging | 40% |

| Building & Construction | 14% |

| Electrical & Electronics | 20% |

| Automotive | 26% |

- Packaging - The packaging sector holds 40% shares, representing the largest and most important segment of the market, bolstered by substantial demand across industries such as food, beverage, healthcare, and e-commerce.

- Building & construction - The building and construction sector holds 14% share, plays a key role in the market, supported by the need for durable, lightweight, and energy-efficient materials that provide cost-effective alternatives to traditional options like metal, wood, and concrete.

- Electrical & electronics - The electrical and electronics (E&E) sector, holding 20% shares, plays an important role in the market, driven by the need for lightweight and durable materials used in consumer electronics, 5G infrastructure, and electric vehicles (EVs).

- Automotive - The automotive sector is a key contributor, holding 26% shares, as it generates demand for such materials to enhance fuel efficiency and support the growing production of EV components.

U.S. Plastics Market, By Application, 2025 (%)

| Segments | Shares (%) |

| Injection Molding | 45% |

| Blow Molding | 20% |

| Roto Molding | 21% |

| Compression Molding | 14% |

- Injection Molding - The injection molding segment plays a dominant role in the market, holding 45% shares, serving as the primary high-volume manufacturing method for industries such as packaging, automotive, and medical devices.

- Blow Molding - the blow molding segment, which holds 20% shares, is important to the market, recognized for its efficiency in producing lightweight, durable, and cost-effective hollow plastic components.

- Roto Molding - The roto molding sector plays a vital role in the U.S. plastics industry, holds 21% share, by enabling the production of durable, large, and complex hollow parts, such as tanks, containers, and automotive components, through the use of economical tooling.

- Compression Molding - the compression molding segment, which holds 14% share, is significant due to its efficiency in high-volume manufacturing, capability to produce high-strength components, and adaptability for creating complex, large-scale parts.

Top Companies in the U.S. Plastics Market

- ExxonMobil Chemical

- Dow, Inc.

- Chevron Phillips Chemical Co., LLC

- Westlake Chemical

- DuPont

- Celanese Corporation

- Eastman Chemical Company

- Huntsman International LLC

- RTP Company

Segments Covered in the Report

By Product

- Polyethylene (PE)

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

By End-use

- Packaging

- Building & construction

- Electrical & electronics

- Automotive

By Application

- Injection Molding

- Blow Molding

- Roto Molding

- Compression Molding

| Product | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Polyethylene (PE) | 32.64 | 33.61 | 34.62 | 35.65 | 36.71 | 37.80 | 38.93 | 40.08 | 41.27 | 42.49 | 43.75 |

| Polypropylene (PP) | 24.96 | 26.06 | 27.20 | 28.39 | 29.64 | 30.93 | 32.28 | 33.69 | 35.16 | 36.69 | 38.28 |

| Polyurethane (PU) | 17.28 | 18.10 | 18.96 | 19.85 | 20.79 | 21.77 | 22.79 | 23.85 | 24.97 | 26.13 | 27.34 |

| Polyvinyl Chloride (PVC) | 21.12 | 21.68 | 22.25 | 22.84 | 23.44 | 24.06 | 24.69 | 25.33 | 25.99 | 26.66 | 27.34 |

| End-use | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Packaging | 38.40 | 39.98 | 41.62 | 43.33 | 45.12 | 46.97 | 48.90 | 50.90 | 52.99 | 55.16 | 57.42 |

| Building & Construction | 28.80 | 29.64 | 30.50 | 31.38 | 32.29 | 33.22 | 34.18 | 35.16 | 36.18 | 37.22 | 38.28 |

| Electrical & Electronics | 14.40 | 15.02 | 15.66 | 16.33 | 17.03 | 17.76 | 18.51 | 19.30 | 20.13 | 20.98 | 21.88 |

| Automotive | 14.40 | 14.82 | 15.25 | 15.69 | 16.14 | 16.61 | 17.09 | 17.58 | 18.09 | 18.61 | 19.14 |

Research Methodology

Related Databooks

March 2026

March 2026

April 2026

April 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting