Middle East Minimally Invasive Surgery Market Size is USD 8.39 Billion in 2026

Middle East Minimally Invasive Surgery Market (By Surgical Specialty: General Surgery, Gastrointestinal Surgery, Gynecological Surgery, Urological Surgery, Cardiothoracic Surgery, Orthopedic & Spine Surgery, Neurosurgery, Colorectal Surgery, Bariatric Surgery, Vascular & Endoscopic Surgery, Plastic & Reconstructive Surgery; By Method: Laparoscopic Surgery, Thoracoscopic Surgery/VATS, Robotic-assisted Surgery, Endoscopic Surgery, Catheter-based/Interventional Procedures, Others; By End-use: Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Others) Industry Size, Share, Growth, Trends 2026 to 2035.

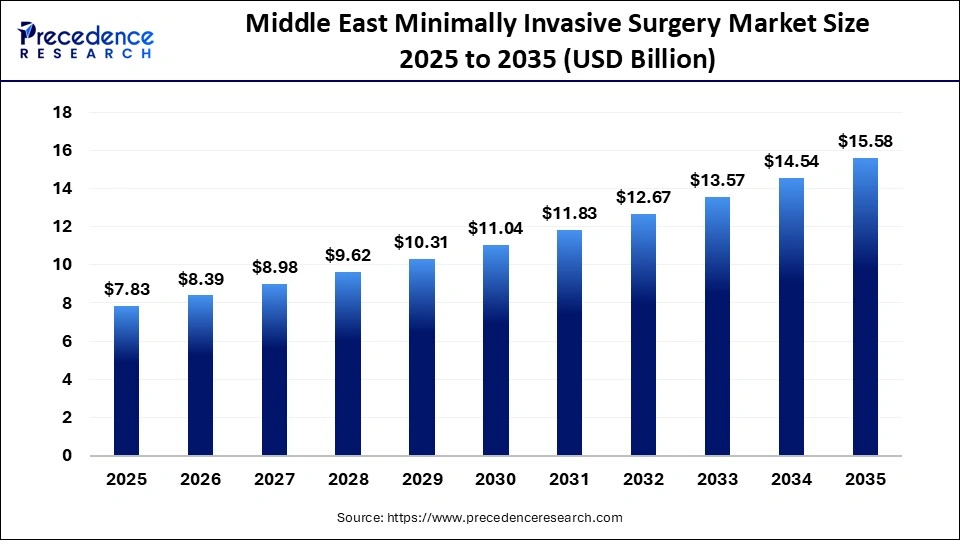

The Middle East minimally invasive surgery market size was estimated at USD 7.83 billion in 2025 and is expanding at a CAGR of 7.12% from 2026 to 2035. The increasing prevalence of lifestyle-related diseases and advancements in technology are driving the market.

Middle East Minimally Invasive Surgery Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 7.83 Billion |

| Market Size in 2026 | USD 8.39 Billion |

| Market Size by 2035 | USD 15.58 Billion |

| CAGR 2026 to 2035 | 7.12% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The minimally invasive surgery (MIS) market includes surgical techniques that use small incisions, specialized instruments, cameras, and robotics to minimize tissue trauma compared to traditional open surgery. MIS offers patients several benefits, including shorter recovery times, reduced pain, fewer complications, and lower healthcare costs. This approach is widely used in areas such as laparoscopy, endoscopy, arthroscopy, interventional cardiology, and robotic-assisted procedures.

In the Middle East, the minimally invasive surgery market is steadily expanding, supported by government-led healthcare reforms, rising rates of lifestyle-related diseases, and increased investments in advanced surgical infrastructure. Countries like Saudi Arabia and the UAE are leading this trend, driven by national health strategies such as Saudi Vision 2030 and the UAE's Centennial 2071 plan.

Middle East Minimally Invasive Surgery Market Share, By Country, 2025

- UAE - The MIS market in the UAE is expected to continue growing as technological advancements, rising patient demand, and a higher prevalence of chronic diseases drive its adoption. The integration of robotic systems, artificial intelligence, and 3D imaging technologies is transforming the landscape of minimally invasive surgery, leading to improved patient outcomes.

Middle East Minimally Invasive Surgery Market Share, By Surgical Speciality, 2025, (%)

| Segments | Shares (%) |

| Gastrointestinal Surgery | 18% |

| Gynaecological Surgery | 10% |

| Bariatric Surgery | 11% |

| Orthopedic and Spine Surgery | 9% |

| Plastic & Reconstructive Surgery | 8% |

| Neurosurgery | 12% |

| Colorectal Surgery | 15% |

| Vascular & Endoscopic Surgery | 2% |

| General Surgery | 5% |

| Urological Surgery | 6% |

| Cardiothoracic Surgery | 4% |

- Gastrointestinal Surgery- It drives the dominant surgical specialty segment, with an 18% share due to growing GI disease prevalence, obesity rates, and the demand for shorter recovery times.

- Gynaecological Surgery- this segment expands with 10% share due to demand for outpatient procedures for hysterectomies, myomectomies, and endometriosis treatment.

- Bariatric Surgery- this segment holds 11% share. This is attributed to the rising prevalence of obesity and related disorders, and an increase in the number of bariatric procedures.

- Orthopedic and Spine Surgery- Rising prevalence of spinal disorders and rising geriatric population contribute to 9% share.

- Plastic & Reconstructive Surgery- an increase in the acceptance of cosmetic procedures among consumers and a growing demand for non-surgical aesthetic procedures accounts for 8% share.

- Neurosurgery- Complex procedures with specialized demand, with a 12% share, support the market but remain below colorectal surgery.

- Colorectal Surgery - Higher procedure volume and growing adoption of advanced surgical techniques, with a 15% share, establishes it as the leading segment.

- Vascular & Endoscopic Surgery - Niche application with lower adoption, with a 2% share, results in minimal overall contribution.

- General Surgery - Broad application but lower specialization demand, with a 5% share, remains limited.

- Urological Surgery- Moderate demand for minimally invasive procedures, with a 6% share, contributes but does not lead.

- Cardiothoracic Surgery - Highly specialized procedures with limited volume, with a 4% share, restrict broader contribution.

Middle East Minimally Invasive Surgery Market Share, By Method, 2025, (%)

| Segments | Shares (%) |

| Robotic-assisted Surgery | 35% |

| Laparoscopic Surgery | 28% |

| Endoscopic Surgery | 15% |

| Catheter-based / Interventional | 10% |

| Thoracoscopic Surgery/VATS | 8% |

| Others | 4% |

- Robotic-assisted Surgery- It drives advanced minimally invasive procedures and higher precision, with a 35% share, and is the leading surgical method.

- Laparoscopic Surgery- It is a majorly performed minimally invasive surgery, with a 28% share, followed by robotic-assisted procedures due to high adoption in abdominal and gynecological procedures.

- Endoscopic Surgery- this segment provides high-definition imaging capabilities that allow for enhanced precision and are used for internal visualization and treatment, with a 15% share.

- Catheter-based / Interventional- mainly used in vascular and cardiac interventions, with a 10% share.

- Thoracoscopic Surgery/VATS- Thoracoscopic Surgery/VATS, with a 8% share, contributes but does not surpass leading segments.

- Others- Includes various smaller applications, with a 4% share, result in moderate contribution.

Middle East Minimally Invasive Surgery Market Share, By End Use, 2025, (%)

| Segments | Shares (%) |

| Hospitals | 68% |

| Ambulatory Surgical Centers | 15% |

| Specialty Clinics | 12% |

| Others | 5% |

- Hospitals - They drive the largest end-use segment, with a 68% share, as the majority of surgical procedures are carried out in hospitals.

- Ambulatory Surgical Centers - this segment holds 15% share. This segment is rapidly growing due to the rising volume of outpatient procedures.

- Specialty Clinics - provide niche treatments and faster recovery, lower infection risks, advanced technique, with a 12% share.

- Others - Includes various smaller applications, with a 5% share, result in moderate contribution.

Top Companies in the Middle East Minimally Invasive Surgery Market

- Medtronic plc

- Intuitive Surgical

- CMR Surgical

- Smith & Nephew plc

- Renishaw

- Robotics Surgical Systems (UAE)

- Auris Health

- Olympus Corporation

- Siemens Healthineers

- Corindus Vascular Robotics

Segments Covered in the Report

By Surgical Specialty

- General Surgery

- Gastrointestinal Surgery

- Gynecological Surgery

- Urological Surgery

- Cardiothoracic Surgery

- Orthopedic & Spine Surgery

- Neurosurgery

- Colorectal Surgery

- Bariatric Surgery

- Vascular & Endoscopic Surgery

- Plastic & Reconstructive Surgery

By Method

- Laparoscopic Surgery

- Thoracoscopic Surgery/VATS

- Robotic-assisted Surgery

- Endoscopic Surgery

- Catheter-based/Interventional Procedures

- Others

By End-use

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Others

| Method | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Laparoscopic Surgery | 1.36 | 1.53 | 1.70 | 1.79 | 2.08 | 2.19 | 2.34 | 2.45 | 2.66 | 2.78 | 2.86 |

| Thoracoscopic Surgery/VATS | 1.28 | 1.37 | 1.42 | 1.50 | 1.60 | 1.78 | 1.95 | 2.00 | 2.33 | 2.49 | 2.78 |

| Robotic-assisted Surgery | 1.30 | 1.37 | 1.46 | 1.56 | 1.58 | 1.68 | 1.69 | 1.80 | 1.76 | 1.82 | 2.21 |

| Endoscopic Surgery | 1.32 | 1.43 | 1.52 | 1.66 | 1.74 | 1.90 | 2.02 | 2.04 | 2.27 | 2.42 | 2.41 |

| Catheter-based/Interventional Procedures | 1.23 | 1.35 | 1.45 | 1.68 | 1.73 | 1.79 | 2.02 | 2.31 | 2.27 | 2.51 | 2.81 |

| Others | 1.34 | 1.34 | 1.43 | 1.43 | 1.58 | 1.70 | 1.81 | 2.07 | 2.28 | 2.52 | 2.51 |

| End-use | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Hospitals | 1.93 | 2.14 | 2.41 | 2.57 | 2.67 | 3.02 | 3.30 | 3.56 | 3.98 | 4.53 | 4.80 |

| Ambulatory Surgical Centers | 1.95 | 2.14 | 2.31 | 2.38 | 2.50 | 2.62 | 2.76 | 2.90 | 3.05 | 3.10 | 3.52 |

| Specialty Clinics | 1.99 | 2.05 | 2.17 | 2.38 | 2.55 | 2.69 | 2.76 | 2.92 | 3.03 | 3.09 | 3.19 |

| Others | 1.96 | 2.06 | 2.09 | 2.29 | 2.59 | 2.71 | 3.01 | 3.29 | 3.51 | 3.82 | 4.07 |

Research Methodology

Related Databooks

March 2026

March 2026

March 2026

March 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting