Dry Electrode Technology Market Size is USD 141.06 Million in 2026

Dry Electrode Technology Market (By Type: Adhesive Fibrillation Method, Spraying Method,; By Application: Capacitors, Lithium Batteries, Other; By Region: North America, LAMEA, Europe, Asia-Pacific) Industry Size, Share, Growth, Trends 2026 to 2035.

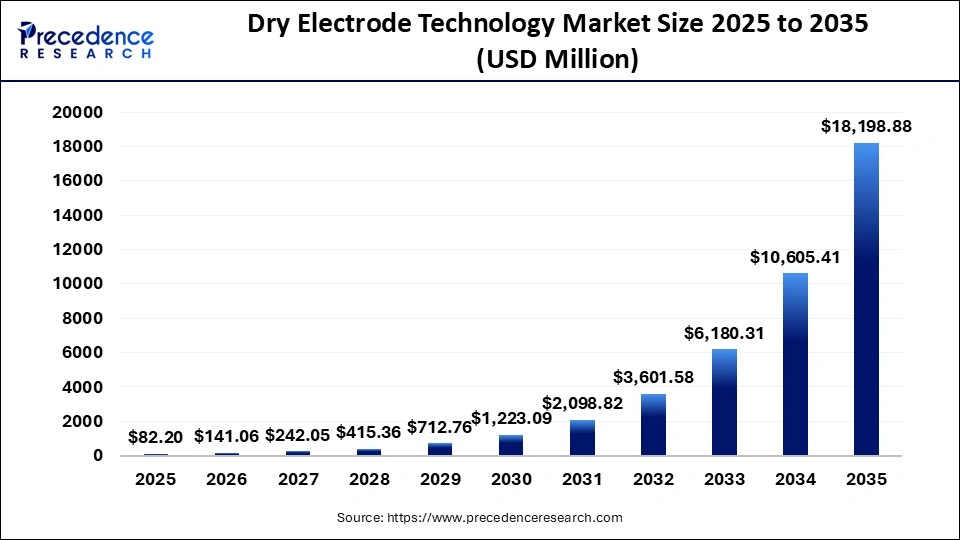

The dry electrode technology market size was estimated at USD 82.20 million in 2025 and is predicted to increase from USD 141.06 million in 2026 to approximately USD 18,198.88 million by 2035, expanding at A CAGR of 71.6% from 2026 to 2035. The market is driven by lower-cost, more sustainable electric vehicle batteries.

Dry Electrode Technology Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 82.20 Million |

| Market Size in 2026 | USD 141.06 Million |

| Market Size by 2035 | USD 18,198.88 Million |

| CAGR 2026 to 2035 | 71.6% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

Dry electrode technology is rapidly emerging as a game-changing approach to overcome the technical and environmental challenges posed by conventional wet-slurry processes in lithium-ion batteries and solid-state batteries. By eliminating the use of solvents, this method significantly reduces energy consumption and environmental impacts, while also enabling the production of thick, high-energy-density electrodes with improved mechanical stability.

Companies such as Tesla and LG Energy Solution are making substantial investments in this technology. Industry analysis projects that by 2030, if just 10% of battery production uses dry coating, the industry could save 480,000 tons of CO2 emissions annually. This represents a meaningful step toward building a sustainable energy future.

The momentum for dry electrode processing is gaining traction as battery manufacturers face the dual challenges of scaling up capacity and reducing manufacturing energy requirements, while also minimizing supply chain risks. This technology directly addresses these challenges by reducing solvent handling, lowering abatement needs, and potentially allowing for thicker electrodes without the cracking and delamination issues often seen with traditional wet coating methods. However, it does introduce new complexities, such as powder handling, binder fibrillation control, calendering windows, and dust management, which require different engineering expertise and new quality control metrics.

The increasing shift toward sustainable energy sources and the demand for high-performance batteries are pushing manufacturers to innovate in electrode technologies. This includes a growing focus on developing dry electrode solutions that offer enhanced performance while reducing environmental impact. The demand for dry electrode technology is being driven by a strong emphasis on lowering the carbon footprint associated with traditional manufacturing processes. As industries work to comply with stringent environmental regulations, the transition to dry electrode technology presents a viable solution that minimizes waste and energy consumption during production.

Global battery companies are intensifying their efforts to establish themselves in the emerging dry electrode technology market. This innovative approach, which offers significant cost reductions and environmental benefits over traditional wet processes, has become a key area of competition among industry giants. The race to commercialize this technology features major players like Tesla, Panasonic, CATL, and several Korean firms leading the charge.

Dry Electrode Technology Market Share, By Region, 2025 (%)

| Regions | Shares (%) |

| North America | 50% |

| Europe | 25% |

| Asia Pacific | 15% |

| Latin America | 5% |

| Middle East & Africa | 5% |

- North America - Dominates with 50% due to the region's strong presence in electronics manufacturing, automotive (EV), and renewable energy sectors that rely heavily on advanced electrode technology.

- Europe - Does not dominate with 25%, but still plays a significant role due to its strong automotive and battery sectors, particularly in the transition to electric vehicles and renewable energy storage.

- Asia Pacific - Gaining momentum with 15% as the region sees rapid growth in the electronics and electric vehicle industries, contributing to a surge in demand for lithium batteries.

- Latin America - Does not dominate with 5%, representing a smaller portion of the market as demand in this region is still developing.

- Middle East & Africa - Does not dominate with 5%, with limited market penetration compared to other regions.

Dry Electrode Technology Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| Adhesive Fibrillation Method | 60% |

| Spraying Method | 40% |

- Adhesive Fibrillation Method - Dominates with 60% due to its widespread use in dry electrode technology for efficient, high-quality performance in a variety of applications.

- Spraying Method - Gaining momentum with 40% as it offers flexibility and is increasingly used in advanced applications, particularly for large-scale manufacturing and low-cost production.

Dry Electrode Technology Market Share, By Application, 2025 (%)

| Segments | Shares (%) |

| Capacitors | 45% |

| Lithium Batteries | 40% |

| Other | 10% |

- Capacitors - Dominates with 45% due to the long-established use of dry electrodes in capacitors, driven by their importance in electronic devices, energy storage, and power applications.

- Lithium Batteries - Gaining momentum with 40% as the demand for lithium batteries continues to grow, driven by the rise in electric vehicles (EVs), renewable energy storage, and portable electronic devices.

- Other - Does not dominate with 10%, but this category includes niche applications where dry electrode technology is used in specialized fields.

Top Companies of Dry Electrode Technology Market

- Tesla

- LiCAP Technologies

- Sakuu

- LG

- AM Batteries

- Tsingyan Electronic

- Panasonic

- PowerCO

Segments Covered in the Report

By Type

- Adhesive Fibrillation Method

- Spraying Method

By Application

- Capacitors

- Lithium Batteries

- Other

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

| Type | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Adhesive Fibrillation Method | 49.32 | 83.22 | 140.39 | 236.75 | 399.14 | 672.70 | 1133.36 | 1908.84 | 3213.76 | 5408.76 | 9099.44 |

| Spraying Method | 32.88 | 57.83 | 101.66 | 178.60 | 313.61 | 550.39 | 965.46 | 1692.74 | 2966.55 | 5196.65 | 9099.44 |

| Application | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Capacitors | 36.99 | 62.06 | 104.08 | 174.45 | 292.23 | 489.24 | 818.54 | 1368.60 | 2286.71 | 3817.95 | 6369.61 |

| Lithium Batteries | 32.88 | 57.83 | 101.66 | 178.60 | 313.61 | 550.39 | 965.46 | 1692.74 | 2966.55 | 5196.65 | 9099.44 |

| Other | 12.33 | 21.16 | 36.31 | 62.30 | 106.91 | 183.46 | 314.82 | 540.24 | 927.05 | 1590.81 | 2729.83 |

| Region | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| North America | 41.10 | 69.12 | 116.18 | 195.22 | 327.87 | 550.39 | 923.48 | 1548.68 | 2595.73 | 4348.22 | 7279.55 |

| Europe | 20.55 | 34.56 | 58.09 | 97.61 | 163.93 | 275.20 | 461.74 | 774.34 | 1297.86 | 2174.11 | 3639.78 |

| Asia-Pacific | 12.33 | 22.57 | 41.15 | 74.76 | 135.42 | 244.62 | 440.75 | 792.35 | 1421.47 | 2545.30 | 4549.72 |

| Latin America | 4.11 | 7.05 | 12.10 | 20.77 | 35.64 | 61.15 | 104.94 | 180.08 | 309.02 | 530.27 | 909.94 |

| Middle East & Africa | 4.11 | 7.05 | 12.10 | 20.77 | 35.64 | 61.15 | 104.94 | 180.08 | 309.02 | 530.27 | 909.94 |

Research Methodology

Related Databooks

April 2026

April 2026

April 2026

April 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting