Middle East Orthotics Market Size is USD 205.65 Million in 2026

Middle East Orthotics Market (By Type: Upper Limb Orthotics, Lower Limb Orthotics, Spinal Orthotics; By Distribution Channel: Direct Institutional Sales, Retail Sales, E-commerce Platforms; By End Use: Hospitals, Ambulatory Surgical Centers, Rehabilitation Centers; By Application/Indication: Musculoskeletal Disorders, Sports Injuries, Post-operative Rehabilitation, Chronic Conditions; By Material: Thermoplastics & Carbon Fiber Composites, Foam & Silicone-based Materials, Leather & Metal Supports, Advanced Lightweight Bio-composites) Industry Size, Share, Growth, Trends 2026 to 2035.

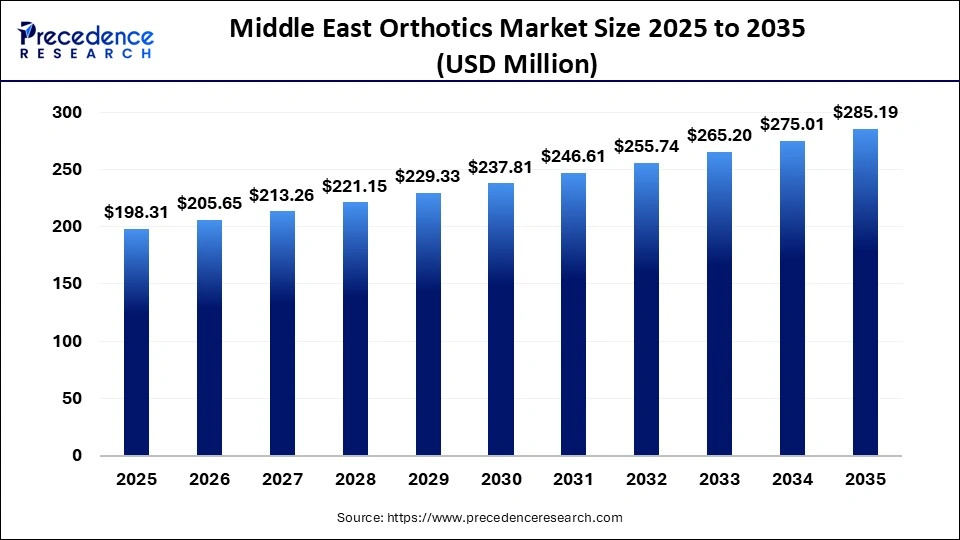

The Middle East orthotics market size was estimated at USD 198.31 million in 2025 and is predicted to increase from USD 205.65 million in 2026 to approximately USD 285.19 million by 2035, expanding at a CAGR of 3.7% from 2026 to 2035. Rising musculoskeletal issues and an aging population are expanding the market.

Middle East Orthotics Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 198.31 Million |

| Market Size in 2026 | USD 205.65 Million |

| Market Size by 2035 | USD 285.19 Million |

| CAGR 2026 to 2035 | 3.7% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

In the orthotics market in the Middle East, there has been a marked increase in the demand for customized and prefabricated devices, signifying a heightened awareness of the importance of mobility and rehabilitation in healthcare. Recent trends indicate the integration of 3D printing and CAD/CAM technologies for personalized orthoses, alongside the expansion of private healthcare facilities and enhanced insurance coverage in select GCC countries, which further propels market growth.

The Middle East Orthotics Market, By Country, 2025

- The UAE- The orthotics market in the UAE is experiencing the rising adoption of minimally invasive procedures. Patients are choosing less invasive surgical techniques that provide faster recovery times, lower pain, and minimal scarring, which are driving the demand.

The Middle East Orthotics Market Share, By Type, 2025, (%)

| Segments | Shares (%) |

| Upper Limb Orthotics | 43% |

| Lower Limb Orthotics | 35% |

| Spinal Orthotics | 22% |

- Upper limb orthotics - upper limb orthotics lead the market with a 43% share, fueled by the high prevalence of upper limb injuries and the associated rehabilitation requirements.

- Lower limb orthotics- The lower limb orthotics segment comprises 35% of the market and is growing due to the rising incidence of spinal disorders and posture-related conditions.

- Spinal Orthotics- The spinal orthotics segment represents a significant 22% of the market, reflecting strong demand for mobility support.

The Middle East Orthotics Market Share, By Distribution Channels, 2025, (%)

| Segments | Shares (%) |

| Direct Institutional Sales | 49% |

| Retail Sales | 34% |

| E-commerce Platforms | 17% |

- Direct Institutional Sales- direct institutional sales prevail as the leading avenue with a 49% share, driven by substantial procurement from hospitals and healthcare institutions.

- Retail Sales- Retail sales hold a 34% market share, which caters to accessibility through medical stores, and are increasingly incorporating trends for customization to enhance comfort and fit.

- E-commerce Platforms- E-commerce platforms are increasingly attractive, accounting for 17% of the market, due to the rise of digital adoption and the convenience of purchasing medical devices online.

The Middle East Orthotics Market Share, By End Use, 2025, (%)

| Segments | Shares (%) |

| Hospitals | 57% |

| Ambulatory Surgical Centers | 28% |

| Rehabilitation Centers | 15% |

- Hospitals- the hospitals segment dominates the market with a 57% share due to high patient inflow and the availability of specialized treatment facilities.

- Ambulatory Surgical Centers- Ambulatory surgical centers are also gaining traction, representing 28% of the market as they facilitate outpatient procedures and a shift toward minimally invasive, same-day surgical approaches.

- Rehabilitation Centers - Rehabilitation centers focus on recovery and therapy services, encompassing a 15% market share. The growing awareness of specialized rehabilitation services, paired with improved healthcare insurance coverage, further enhances market demand.

The Middle East Orthotics Market Share, By Application, 2025, (%)

| Segments | Shares (%) |

| Musculoskeletal Disorders | 48% |

| Sports Injuries | 21% |

| Post-operative Rehabilitation | 17% |

| Chronic Conditions | 14% |

- Musculoskeletal Disorders- musculoskeletal disorders establish themselves as the leading segment with a 48% market share, attributed to a high incidence of bone and joint conditions.

- Sports Injuries- Sports injuries contribute significantly comprises 21% of the market as active populations increasingly encounter injuries.

- Post-operative Rehabilitation- post-operative rehabilitation represents a 17% share, arising from a rise in surgical procedures necessitating essential recovery support.

- Chronic Conditions- chronic conditions require long-term support devices and hold a 14% market share, driven by the rising prevalence of diabetes, obesity, and musculoskeletal disorders.

The Middle East Orthotics Market Share, By Material, 2025, (%)

| Segments | Shares (%) |

| Thermoplastics & Carbon Fiber Composites | 57% |

| Foam & Silicone-Based Materials | 20% |

| Advanced Lightweight Bio-Composites | 13% |

| Leather & Metal Supports | 10% |

- Thermoplastics & Carbon Fiber Composites- this segment holds a dominant share of 57% as they are Lightweight, durable, and customizable, establishing this as the leading material segment.

- Foam & Silicone-Based Materials- this material provides comfort and cushioning benefits and therefore accounts for a 20% share, supporting demand.

- Advanced Lightweight Bio-Composites- this segment holds 13% share due to Innovation in sustainable and high-performance materials, which is driving growth in this segment.

- Leather & Metal Supports- this segment accounts for a 10% share, driven by the need for durable, customizable, and traditional materials.

Top Companies in the Middle East Orthotics Market

- Blatchford Limited (CBPE Capital)

- Aetrex Middle East

- Ottobock

- Össur

- Bauerfeind Polyclinic.

- Create it REAL A/S

- Steeper Group

- HealTec

- Spentys

- Allard USA Inc. (Allard Support For Better Life AB)

Segments Covered in the Report

By Type

- Upper Limb Orthotics

- Wrist/hand orthoses

- Elbow orthoses

- Shoulder orthoses

- Lower Limb Orthotics

- Foot orthoses

- Knee orthoses

- Hip orthoses

- Spinal Orthotics

- Cervical braces & collars

- Thoracic & lumbar supports (TLSOs, LSOs)

- Scoliosis braces

By Distribution Channel

- Direct Institutional Sales

- Retail Sales

- E-commerce Platforms

By End Use

- Hospitals

- Ambulatory Surgical Centers

- Rehabilitation Centers

By Application/Indication

- Musculoskeletal Disorders

- Sports Injuries

- Post-operative Rehabilitation

- Chronic Conditions

By Material

- Thermoplastics & carbon fiber composites

- Foam & silicone-based materials

- Leather & metal supports

- Advanced lightweight bio-composites

| End Use | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Hospitals | 103.12 | 106.53 | 110.04 | 113.67 | 117.42 | 121.28 | 125.28 | 129.40 | 133.66 | 138.06 | 142.59 |

| Ambulatory Surgical Centers | 35.70 | 37.43 | 39.24 | 41.13 | 43.11 | 45.18 | 47.35 | 49.61 | 51.98 | 54.45 | 57.04 |

| Rehabilitation Centers | 59.49 | 61.70 | 63.98 | 66.34 | 68.80 | 71.34 | 73.98 | 76.72 | 79.56 | 82.50 | 85.56 |

| Application | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Musculoskeletal Disorders | 71.39 | 73.62 | 75.92 | 78.29 | 80.72 | 83.23 | 85.82 | 88.49 | 91.23 | 94.05 | 96.96 |

| Sports Injuries | 35.70 | 37.43 | 39.24 | 41.13 | 43.11 | 45.18 | 47.35 | 49.61 | 51.98 | 54.45 | 57.04 |

| Post-operative Rehabilitation | 43.63 | 45.65 | 47.77 | 49.98 | 52.29 | 54.70 | 57.21 | 59.84 | 62.59 | 65.45 | 68.45 |

| Chronic Conditions | 47.59 | 48.94 | 50.33 | 51.75 | 53.20 | 54.70 | 56.23 | 57.80 | 59.40 | 61.05 | 62.74 |

Research Methodology

Related Databooks

March 2026

March 2026

March 2026

March 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting