Middle East Copper Market Size is USD 1,537.25 Million in 2026

Middle East Copper Market (By Type: Primary Copper, Secondary Copper; By Product: Wire, Rods, Bars & Sections, Flat Rolled Products, Tube, Foil; By End Use: Industrial Equipment, Transport, Infrastructure, Building & Construction, Consumer & General Products, Others) Industry Size, Share, Growth, Trends 2026 to 2035.

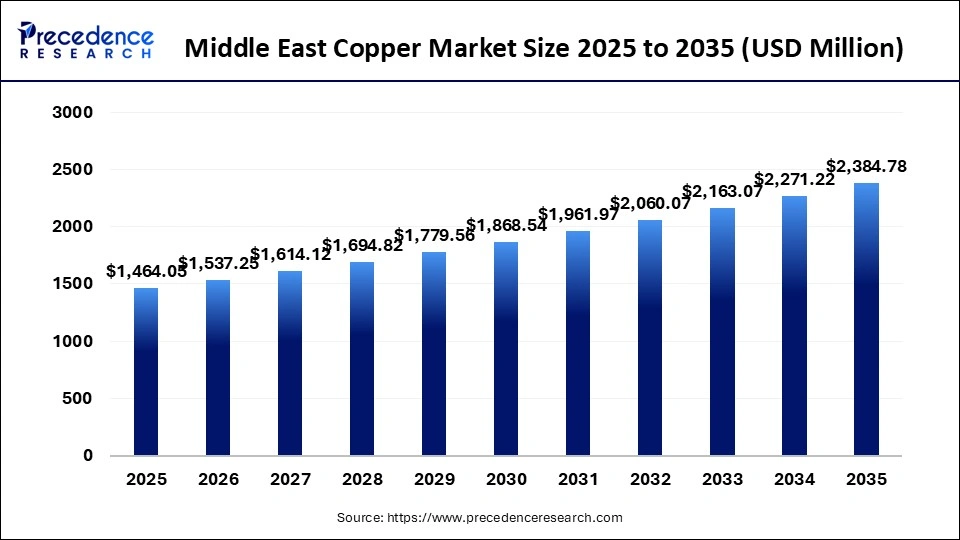

The Middle East copper market size was estimated at USD 1,464.05 million in 2025 and is expanding at a CAGR of 5% from 2026 to 2035. Due to rapid infrastructure development, rising construction activities, and increasing demand from renewable energy and electrical sectors, the government is investing in industrial diversification and urbanisation to support steady market expansion.

Middle East Copper Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 1,464.05 Million |

| Market Size in 2026 | USD 1,537.25 Million |

| Market Size by 2035 | USD 2,384.78 Million |

| CAGR 2026 to 2035 | 5% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

Technological advancements in the Middle East copper market are enhancing efficiency, sustainability, and product quality. Modern extraction and refining techniques, such as solvent extraction, electro-winning, and automation, improve recovery rates while reducing environmental impact. The adoption of digital monitoring systems, AI-driven process optimization, and energy-efficient smelting technologies is streamlining operations.

Additional innovations in recycling methods and the use of smart manufacturing art support circular economic practices and meet the rising demand for high-purity copper in advanced electrical renewable energy applications.

Middle East Copper Market Share, By Country, 2025 (%)

- UAE- Due to strong construction activity, infrastructure projects, and growth in renewable energy initiatives, the country's focus on industrial diversification and smart city development is increasing demand for copper in electrical wiring devices and technology applications, while rising investment in recycling and thread hubs to support market growth.

- Saudi Arabia- Due to large-scale infrastructure projects and industrial expansion, increasing demand from construction, power generation , and the renewable energy sector is boosting copper consumption. Additionally, investments in mining development and downstream industries are strengthening domestic supply and supporting long-term market growth.

Middle East Copper Market Share, By Type, 2025 (%)

| Segments | Shares (%) |

| Primary Copper | 84.50% |

| Secondary Copper | 15.50% |

- Primary Copper- The segment dominated the market with an 84.50% share, due to strong demand for high-quality newly mined copper in construction, electrical infrastructure, and industrial applications. Wear purity and performance are essential.

- Secondary Copper- The segment accounted for 15.50% of the total market share, due to limited recycling infrastructures and lower scrap availability. Though it is gradually growing with an increasing focus on sustainability and cost-effective metal reuse.

Middle East Copper Market Share, By Product, 2025 (%)

| Segments | Shares (%) |

| Wire | 44% |

| Rods, Bars & Sections | 20% |

| Flat Rolled Products | 14% |

| Tube | 13% |

| Foil | 9% |

- Wire- The segment dominated the market with a 44% share, due to high demand from power transmission, construction, and telecommunication sectors where copper wiring is essential for reliable electrical conductivity and infrastructure development.

- Rods, Bars & Sections- The segment accounted for 20% of the total market share, due to steady demand from construction, manufacturing, and industrial machinery, where these forms are widely used for structural and fabrication purposes.

- Flat Rolled Products- The segment accounted for 14% of the total market share, due to demand. Automotive components, electronics, and construction wear sheets and plates are valued for flexibility, durability, and conductivity.

- Tube- The segment accounted for 13% of the total market share, due to demand from HVAC system plumbing and refrigeration systems, where copper tubes are preferred for durability, corrosion resistance, and efficient heat transfer properties.

- Foil- The segment accounted for 9% of the total market share. Due to the rising use of electronic batteries and electrical components, we need thin copper layers that are essential for conductivity and precision applications.

Middle East Copper Market Share, By End Use, 2025 (%)

| Segments | Shares (%) |

| Building & Construction | 27% |

| Infrastructure | 22% |

| Industrial Equipment | 18% |

| Transport | 14% |

| Consumer & General Products | 12% |

| Others | 7% |

- Building & Construction- The segment dominated the market with a 27% share, due to rapid urbanization, large infrastructure projects, and high demand for copper in wiring, plumbing, and structural applications.

- Infrastructure- The segment accounted for 22% of the total market share, due to ongoing investment in power grids, transportation networks, and utilities, where corporate is essential for durability, conductivity, and long-term performance.

- Industrial Equipment- The segment accounted for 18% of the total market share, due to demand for copper in machinery, motors, and manufacturing tools valued for its excellent conductivity, corrosion resistance, and mechanical strength.

- Transport- The segment accounted for 14% of the total market share, due to copper's critical role in automotive wiring, electric vehicles, and railway systems, where viability, conductivity, and durability are essential.

- Consumer & General Products- The segment accounted for 12% of the total market share, due to demand for copper in household appliance electronics and everyday products requiring conductivity, durability, and corrosion resistance.

Top Companies in the Middle East Copper Market

- Al-Masane Al Kobra Mining Company (AMAK)

- Alara Resources Limited

- Mawarid Mining LLC

- Minerals Development Oman (MDO)

- National Iranian Copper Industries Company (NICICO)

- Saudi Arabian Mining Company (Ma'aden)

Segments Covered in the Report

By Type

- Primary Copper

- Secondary Copper

By Product

- Wire

- Rods, Bars & Sections

- Flat Rolled Products

- Tube

- Foil

By End Use

- Industrial Equipment

- Transport

- Infrastructure

- Building & Construction

- Consumer & General Products

- Others

| Type | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Primary Copper | 1000.00 | 1049.50 | 1098.94 | 1148.09 | 1198.92 | 1250.37 | 1303.41 | 1357.99 | 1414.07 | 1471.58 | 1530.49 |

| Secondary Copper | 464.05 | 487.75 | 514.17 | 545.68 | 579.54 | 616.02 | 657.35 | 700.80 | 747.66 | 798.24 | 852.82 |

| Product | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Wire | 420.00 | 439.00 | 459.85 | 481.64 | 503.94 | 527.14 | 551.30 | 576.47 | 602.64 | 629.85 | 658.15 |

| Rods, Bars & Sections | 320.00 | 333.60 | 348.24 | 363.94 | 380.75 | 398.67 | 417.73 | 437.92 | 459.31 | 481.98 | 505.97 |

| Flat Rolled Products | 315.00 | 329.49 | 345.97 | 363.65 | 382.63 | 403.01 | 424.87 | 448.31 | 473.43 | 500.33 | 529.10 |

| Tube | 235.00 | 246.75 | 259.08 | 271.92 | 285.32 | 299.24 | 313.71 | 328.77 | 344.45 | 360.77 | 377.76 |

| Foil | 174.05 | 188.41 | 200.96 | 212.62 | 226.52 | 238.47 | 252.15 | 266.92 | 281.90 | 298.89 | 311.24 |

Research Methodology

Related Databooks

March 2026

March 2026

April 2026

April 2026

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting