Middle East High Pressure Seals Market Size is USD 351.08 Million in 2026

Middle East High Pressure Seals Market (By Material: Metal, TPU, HNBR, Fluoroelastomers, EPDM, Others; By End Use: Automotive, Electrical & Electronics, Marine & Rail, Industrial & Manufacturing, Aerospace, Oil & Gas, Chemicals & Petrochemicals, Others) Industry Size, Share, Growth, Trends 2026 to 2035.

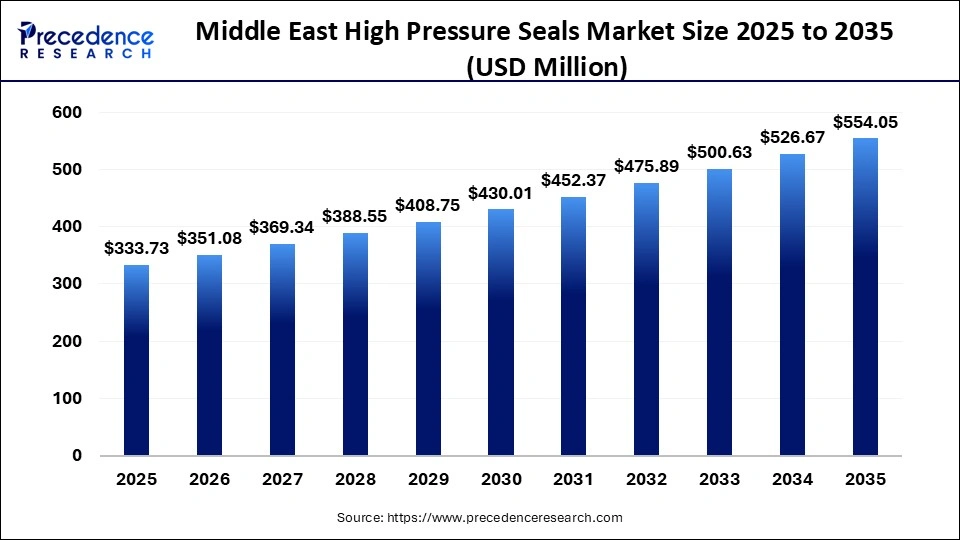

The Middle East high pressure seals market size was estimated at USD 333.73 million in 2025 and is expanding at a CAGR of 5.2% from 2026 to 2035. Due to expanding oil and gas exploration, rising industrialization and infrastructure projects, increased demand for durable sealing solutions in harsh environments, and advancements in material technology, also support for steady market expansion.

Middle East High Pressure Seals Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 333.73 Million |

| Market Size in 2026 | USD 351.08 Million |

| Market Size by 2035 | USD 554.05 Million |

| CAGR 2026 to 2035 | 5.20% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

Technological advancements in the Middle East. The high-pressure seals market is focused on improving durability and performance in extreme conditions. Manufacturers are adopting advanced materials like PTFE, PEEK, and nanocomposites for better resistance to heat, pressure, and corrosion. Smart seals with embedded Sensors enable real-time monitoring and predictive maintenance, reducing downtime.

Additionally, innovations such as self-lubricating designs, metal seals, and hybrid Composites Enhance efficiency and extended operational life in demanding industries like oil and gas.

Middle East High Pressure Seals Market Share, By Country, 2025 (%)

- UAE- Due to rapid industrial growth, strong oil and gas operations, and infrastructure development, rising investments in energy desalination and manufacturing sectors increase demand for durable sealing solutions. Additionally, the country's focus on advanced technologies and efficient maintenance practices supports the adaptation of high-performance seals.

- Saudi Arabia- Due to strong oil and gas activities and ongoing industrial expansion, increasing investment in petrochemical projects and energy infrastructures is driving demand for reliable sealing solutions. Additionally, modernization initiatives and harsh operating environments encourage the adoption of advanced high-performance seal technologies across key industries.

Middle East High Pressure Seals Market Share, By Material, 2025 (%)

| Segments | Shares (%) |

| Fluoroelastomers | 27% |

| Metal | 18% |

| EPDM | 16% |

| HNBR | 24% |

| TPU | 15% |

- Fluoroelastomers- The segment dominated the market with a 27% share, due to its excellent resistance to high temperatures and harsh environments, making a number of demanding oil and gas and industrial sealing applications.

- Metal- The segment accounted for 18% of the total market share, due to its superior strength, high pressure tolerance, and reliability in extreme temperatures, making it suitable for critical oil, gas, and heavy industrial applications.

- EPDM- The segment accounted for 16% of the total market share, due to its strong resistance to weathering, seal and chemicals, along with cost-effectiveness, making it suitable for water HVAC, and industrial sealing applications.

- HNBR- The segment accounted for 14% of the total market share, due to its excellent resistance to heat, oil, and wear, making it suitable for demanding oil and gas and automotive sealing applications.

- TPU- The segment accounted for 10% of the total market share, due to its high flexibility, abrasion resistance, and durability under pressure, making it suitable for dynamic sealing applications in industrial and hydraulic systems.

Middle East High Pressure Seals Market Share, By End-Use, 2025 (%)

| Segments | Shares (%) |

| Automotive | 37% |

| Oil & Gas | 15% |

| Industrial & Manufacturing | 14% |

| Electrical & Electronics | 10% |

| Marine & Rail | 8% |

| Aerospace | 7% |

| Chemicals & Petrochemicals | 9% |

- Automotive- The segment dominated the market with a 37% share in Pakistan due to rising vehicle production demand for durable sealing in engines and hydraulics , and the need for high-pressure temperature resistance components ensuring performance and safety.

- Oil & Gas- The segment accounted for 15% of the total market share, due to continuous exploration, drilling, and refining activities where high-pressure seals are essential for preventing leaks and ensuring safe operations.

- Industrial & Manufacturing- The segment accounted for 14% of the total market share, due to increasing automation and machinery use. High-pressure seals are needed to ensure efficiency, prevent leaks, and maintain equipment reliability.

- Electrical & Electronics- The segment accounted for 10% of the total market share, due to rising demand for protective seals and insensitive components ensuring insulation, moisture resistance, and reliability in high-performance electronic systems.

- Marine & Rail- The segment accounted for 8% of the total market share, due to demand for durable seals in harsh, high-pressure environments, ensuring leak prevention, corrosion resistance and reliable performance in transport systems.

- Aerospace- The segment accounted for 7% of the total market share, due to the need for high-performance seals that withstand extreme pressure and temperature, ensuring safety, reliability, and efficiency in aircraft systems and components.

- Chemicals & Petrochemicals- The segment accounted for 9% of the total market share, due to strong demand for seals that resist aggressive chemicals' high pressure and temperature, ensuring safe, leak-free processing operations.

Top Companies in the Middle East High Pressure Seals Market

- EagleBurgmann Saudi Arabia

- AESSEAL Saudi Arabia Co. Ltd.

- Arabian Seals Company Ltd. (ASC)

- Sealmatic Oman

- Hydro Serve Pumps & Machinery Trading LLC

- QMS Seals

- Quantech Seal Manufacturing LLC

- Precision Polymer Engineering (PPE LLC)

- Hydrofit Engineering Sharjah

- Bliss Anand KSA

Segments Covered in the Report

By Material

- Metal

- TPU

- HNBR

- Fluoroelastomers

- EPDM

- Others

By End Use

- Automotive

- Electrical & Electronics

- Marine & Rail

- Industrial & Manufacturing

- Aerospace

- Oil & gas

- Chemicals & Petrochemicals

- Others

| Material | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Metal | 60.07 | 62.84 | 65.74 | 68.77 | 71.94 | 75.25 | 78.71 | 82.33 | 86.11 | 90.06 | 94.19 |

| TPU | 40.05 | 42.66 | 45.43 | 48.37 | 51.50 | 54.83 | 58.36 | 62.10 | 66.08 | 70.31 | 74.80 |

| HNBR | 53.40 | 56.35 | 59.46 | 62.75 | 66.22 | 69.88 | 73.74 | 77.81 | 82.10 | 86.64 | 91.42 |

| Fluoroelastomers | 90.11 | 95.14 | 100.46 | 106.07 | 112.00 | 118.25 | 124.85 | 131.82 | 139.18 | 146.94 | 155.14 |

| EPDM | 46.72 | 48.80 | 50.97 | 53.23 | 55.59 | 58.05 | 60.62 | 63.29 | 66.08 | 68.99 | 72.03 |

| Others | 43.38 | 45.29 | 47.28 | 49.35 | 51.50 | 53.75 | 56.09 | 58.53 | 61.08 | 63.73 | 66.49 |

| End Use | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Automotive | 46.72 | 49.50 | 52.45 | 55.56 | 58.86 | 62.35 | 66.05 | 69.96 | 74.09 | 78.47 | 83.11 |

| Electrical & Electronics | 33.37 | 35.64 | 38.04 | 40.60 | 43.33 | 46.23 | 49.31 | 52.59 | 56.07 | 59.78 | 63.72 |

| Marine & Rail | 26.70 | 28.26 | 29.92 | 31.67 | 33.52 | 35.48 | 37.55 | 39.74 | 42.05 | 44.50 | 47.09 |

| Industrial & Manufacturing | 60.07 | 63.20 | 66.48 | 69.94 | 73.58 | 77.40 | 81.43 | 85.66 | 90.11 | 94.80 | 99.73 |

| Aerospace | 23.36 | 24.75 | 26.22 | 27.78 | 29.43 | 31.18 | 33.02 | 34.98 | 37.05 | 39.24 | 41.55 |

| Oil & gas | 73.42 | 76.89 | 80.52 | 84.31 | 88.29 | 92.45 | 96.81 | 101.36 | 106.13 | 111.13 | 116.35 |

| Chemicals & Petrochemicals | 43.38 | 45.47 | 47.64 | 49.93 | 52.32 | 54.83 | 57.45 | 60.20 | 63.08 | 66.10 | 69.26 |

| Others | 26.70 | 27.38 | 28.07 | 28.75 | 29.43 | 30.10 | 30.76 | 31.41 | 32.04 | 32.65 | 33.24 |

Research Methodology

Related Databooks

March 2026

April 2026

April 2026

April 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting