U.S. Flooring Market Size is USD 24.02 Billion in 2026

U.S. Flooring Market (By Product: Ceramic Tiles, Vitrified (Porcelain) Tiles, Carpet, Vinyl, Luxury Vinyl Tiles (LVT), Linoleum/Rubber, Wood & Laminate, Natural Stone, and Others; By End-use: Residential and Non-Residential) Industry Size, Share, Growth, Trends 2026 to 2035.

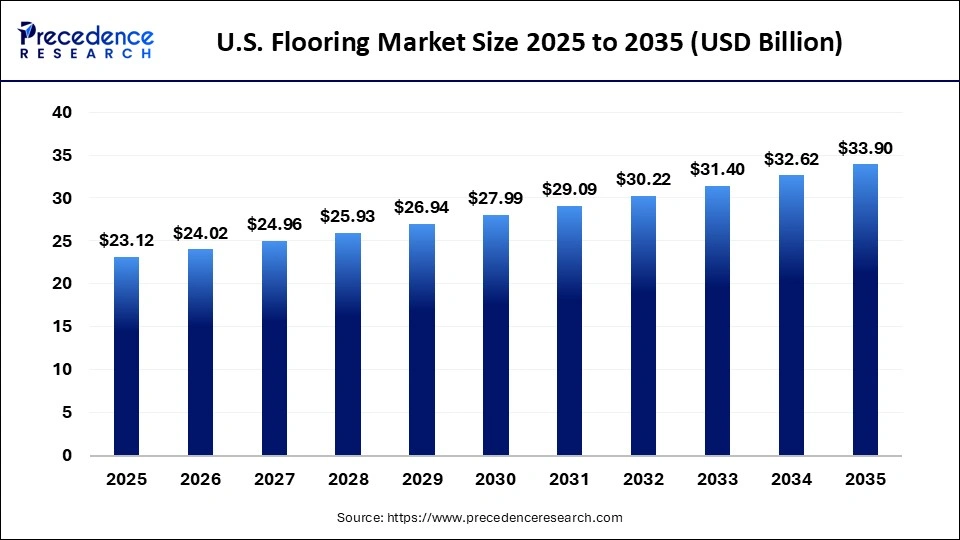

The U.S. flooring market size is estimated at USD 23.12 billion in 2025 and is predicted to increase from USD 24.02 billion in 2026 to approximately USD 33.90 billion by 2035, expanding at a CAR of 3.9% from 2026 to 2035. Rising residential and commercial construction, increasing renovation activities, and growing demand for durable, aesthetically appealing, and sustainable loading solutions are key factors driving the growth of the U.S. flooring market.

U.S. Flooring Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 23.12 Billion |

| Market Size in 2026 | USD 24.02 Billion |

| Market Size by 2035 | USD 33.90 Billion |

| CAGR 2026 to 2035 | 3.9% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The U.S. flooring market refers to the production and sale of materials like tiles, wood, and vinyl, driven by housing demand, renovation trends, urbanization, technological advancements, and increasing preference for durable, cost-effective, and aesthetically appealing flooring solutions.

Technological advancements in the U.S. flooring industry have significantly improved material quality and manufacturing decisions, leading to innovations such as engineered wood and advanced resilient flooring like luxury vinyl tiles. These developments enable highly realistic textures and finishes that loosely resemble natural stone and hardwood while also enhancing durability, quarter resistance, and maintenance.

Additionally, manufacturers are introducing customizable and design-focused flooring solutions with unique patterns and functional features meeting evolving consumers' preferences for both aesthetic and performance.

U.S. Flooring Market Share, By Product, 2025 (%)

| Segments | Shares (%) |

| Ceramic Tiles | 8.40% |

| Vitrified (Porcelain) Tilelets | 9.60% |

| Carpet | 41.20% |

| Vinyl | 7.30% |

| Luxury Vinyl Tiles (LVT) | 5.00% |

| Linoleum/Rubber | 3.20% |

| Wood & Laminate | 10.10% |

| Natural Stone | 13.00% |

| Others | 2.30% |

- Ceramic Tiles- Holding an 8.40% market share, moderate adoption restricts its dominance, as rising competition from more durable and premium flooring options is gradually influencing consumer preference.

- Vitrified (Porcelain) Tilelets- Strong demand for low-maintenance, highly durable premium flooring, accounting for a 9.6% share, is driving a robust growth in both residential and commercial markets.

- Carpet- Comfort, affordability, and hassle-free installation are driving strong demand, giving this flooring segment a dominant 41.2% share in the market.

- Vinyl- Holding a modest 7.30% share, its overall market position is constrained by consumers' shift towards higher-end, more visually appealing flooring materials.

- Luxury Vinyl Tiles (LVT)- The segment holding a 5% share, is experiencing Significant growth as consumers increasingly seek flooring that is affordable, long-lasting, and visually appealing.

- Linoleum/Rubber- The segment 3.20% share reflects its limited appeal, as it is primarily suited for niche and specialized uses.

- Wood & Laminate- With a 10.10% market share, its premium look is offset by higher costs and maintenance requirements, restricting border market adoption.

- Natural Stone- Although valued for its premium quality and durability, high installation expenses and its 13% share keep it from overtaking the market leaders.

- Others- Holding a 2.30% market share, its use in niche applications is limited, leading to a negligible effect on the broader market.

U.S. Flooring Market Share, By End-Use, 2025 (%)

| Segments | Shares (%) |

| Residential | 52.10% |

| Non-Residential | 47.90% |

- Residential- This segment leads the market with a 52.1% share, supported by booming housing demand, active renovations, and growing consumer focus on interior aesthetics.

- Non-Residential- This segment is rapidly expanding, supported by 47.9% share and rising investment in commercial, office, and public infrastructure projects.

Top Companies in the U.S. Flooring Market

- Mohawk Industries, Inc.

- Tarkett

- Forbo Flooring North America

- Interface, Inc.

- EGGER Group

- LG Hausys, Ltd.

- Shaw Industries Group, Inc.

- Mannington Mills, Inc.

- Armstrong Flooring

- Gerflor

- Polyflor Ltd.

- Porcelanosa

- Milliken & Company

- Beaulieu International Group

- Congoleum

Segments Covered in the Report

By Product

- Ceramic Tiles

- Vitrified (Porcelain) Tiles

- Carpet

- Vinyl

- Luxury Vinyl Tiles (LVT)

- Linoleum/Rubber

- Wood & Laminate

- Natural Stone

- Others

By End-use

- Residential

- Non-Residential

| Product | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Ceramic Tiles | 2.77 | 2.86 | 2.95 | 3.03 | 3.13 | 3.22 | 3.32 | 3.41 | 3.52 | 3.62 | 3.73 |

| Vitrified (Porcelain) Tiles | 2.31 | 2.38 | 2.45 | 2.52 | 2.59 | 2.66 | 2.73 | 2.81 | 2.89 | 2.97 | 3.05 |

| Carpet | 6.01 | 6.17 | 6.34 | 6.51 | 6.68 | 6.86 | 7.04 | 7.22 | 7.41 | 7.60 | 7.80 |

| Vinyl | 3.24 | 3.41 | 3.59 | 3.79 | 3.99 | 4.20 | 4.42 | 4.65 | 4.90 | 5.15 | 5.42 |

| Luxury Vinyl Tiles (LVT) | 2.08 | 2.23 | 2.40 | 2.57 | 2.75 | 2.94 | 3.14 | 3.35 | 3.58 | 3.82 | 4.07 |

| Linoleum/Rubber | 1.16 | 1.20 | 1.25 | 1.30 | 1.35 | 1.40 | 1.45 | 1.51 | 1.57 | 1.63 | 1.70 |

| Wood & Laminate | 3.47 | 3.63 | 3.79 | 3.97 | 4.15 | 4.34 | 4.54 | 4.74 | 4.96 | 5.19 | 5.42 |

| Natural Stone | 1.39 | 1.43 | 1.47 | 1.52 | 1.56 | 1.61 | 1.66 | 1.71 | 1.76 | 1.81 | 1.86 |

| Others | 0.69 | 0.71 | 0.72 | 0.74 | 0.75 | 0.77 | 0.79 | 0.80 | 0.82 | 0.83 | 0.85 |

| End Use | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Residential | 12.95 | 13.48 | 14.03 | 14.60 | 15.19 | 15.81 | 16.46 | 17.13 | 17.84 | 18.56 | 19.32 |

| Non-Residential | 10.17 | 10.54 | 10.93 | 11.33 | 11.75 | 12.18 | 12.63 | 13.09 | 13.56 | 14.06 | 14.58 |

Research Methodology

Related Databooks

March 2026

March 2026

April 2026

April 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting