Europe Microfluidics Market Size is USD 13.26 Billion in 2026

Europe Microfluidics Market (By Product: Microfluidic-Based Devices, Microfluidic Components, Chips, Micro-Pumps, Sensors, Others; By Technology: Lab-on-a-Chip, Organ-on-a-Chip, Continuous Flow Microfluidics, Optofluidics and Microfluidics, Acoustofluidics and Microfluidics, Electrophoresis and Microfluidics; By Material Type: Silicon, Glass, Polymer, PDMS, Others; By Application: Medical (Pharmaceuticals, Medical Devices, In-vitro Diagnostics, Others), Non-Medical) Industry Size, Share, Growth, Trends 2026 to 2035.

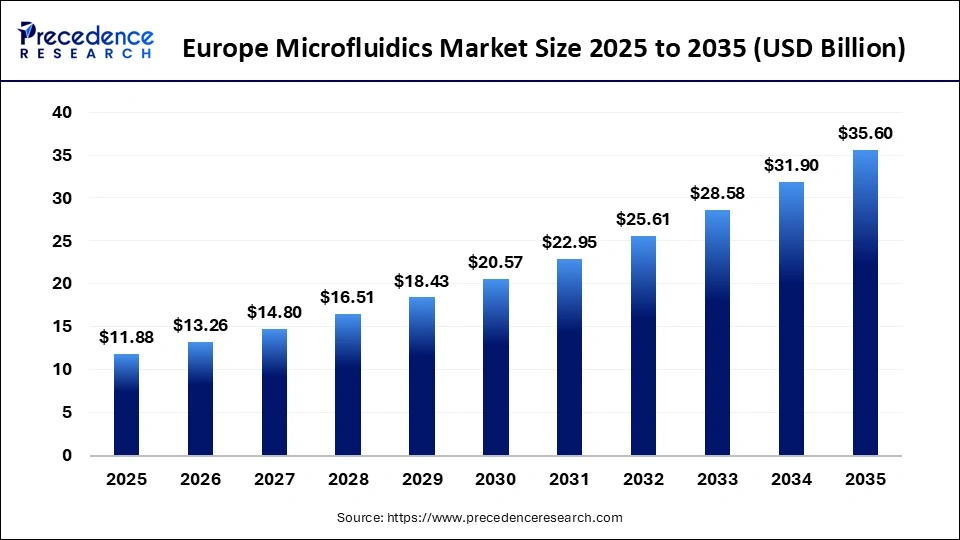

The Europe microfluidics market size was estimated at USD 11.88 billion in 2025 and is expanding at a CAGR of 11.60% from 2026 to 2035. Due to rising demand for point-of-care diagnostics, increasing investment in life science research and advancement in lab-on-chip technologies, expanding applications in drug development and personalized medicines are also driving adoption across the region.

Europe Microfluidics Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 11.88 Billion |

| Market Size in 2026 | USD 13.26 Billion |

| Market Size by 2035 | USD 35.6 Billion |

| CAGR 2026 to 2035 | 11.60% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

Technological advancements in the European microfluidics market are driven by innovations in lab-on-chip and organ-on-a-chip systems, enabling faster and more precise diagnostics. Integration of artificial intelligence and automation improves design efficiency and data analysis. Emerging fabrication techniques like 3D printing and digital manufacturing allow cost-effective, scalable production.

Additionally, the use of advanced materials and nanotechnology enhanced wise performance, while ongoing R & D and collaboration continue to expand applications in healthcare and life sciences.

Europe Microfluidics Market Share, By Country, 2025 (%)

- Germany- Due to strong public research funding, a mature biotechnology sector, and rising demand for lab-on-a-chip solutions, advances in precision engineering Machines , 3D printing, and automation are improving production efficiency. Moreover, active collaboration between academia, industry, and healthcare is accelerating innovation in diagnostics and personalized medicine .

- UK- Due to growing healthcare investments, increasing demand for point -of -care testing, strong government-backed research funding, and ongoing advancement in Lab-on-a-chip Technologies, 3D printing, and sustainable materials that improve manufacturing efficiency and scalability.

Europe Microfluidics Market Share, By Product, 2025 (%)

| SegmentsShares (%) | |

| Microfluidic-Based Devices | 62% |

| Microfluidic Components | 38% |

- Microfluidic-Based Devices- The segment dominated the market with a 62% share due to their high adoption in diagnostic drug testing and resources, and their accuracy. Rapid results and growing use in point-of-care applications significantly drive market demand.

- Microfluidic Components- The segment accounted for 38% of the total market share due to rising demand for pumps, walls, and sensors essential for device functionality. Their widespread use in diagnostic research and lab automation supports steady market growth.

Europe Microfluidics Market Share, By Technology, 2025 (%)

| Segments | Shares (%) |

| Lab-On-A-Chip | 30% |

| Organ-On-A-Chip | 12% |

| Continuous Flow Microfluidics | 18% |

| Opto-Fluidics | 14% |

| Acousto-Fluidics | 10% |

| Electrophoresis Microfluidics | 16% |

- Lab-On-A-Chip- The segment dominated the market with a 30% share, due to its compact design, cost efficiency, and ability to perform rapid multi-step analysis, making it highly valuable in diagnostics and research applications.

- Organ-On-A-Chip- The segment accounted for 12% of the total market share, due to its emerging status, high development costs, and limited commercialisation; however, growing use in drug testing and disease modelling is steadily increasing its adoption.

- Continuous Flow Microfluidics- The segment accounted for 18% of the total market share due to its efficiency in chemical synthesis and sample processing, and its scalability. Precision widespread industrial applications drive adoption.

- Opto-Fluidics- The segment accounted for 14% of the total market share, due to its strong use in advanced sensing, imaging, and diagnostics. However, high cost and technical complexity limit its widespread adoption compared to other technologies. Acousto-Fluidics- The segment accounted for 10% of the total market share. Due to its specialized applications in cell manipulation and diagnostics, high technical complexity, and limited commercialization, it restricts broader adoption despite its innovative potential.

- Electrophoresis Microfluidics- The segment accounted for 16% of the total market share, due to its strong use in DNA analysis, protein separation, and clinical diagnostics, offering high-speed and reliability in laboratory applications.

Europe Microfluidics Market Share, By Material Type, 2025 (%)

| Segments | Shares (%) |

| Silicon | 22% |

| Glass | 30% |

| Polymer | 28% |

| PDMS | 20% |

- Silicon- The segment dominated the market with a 22% share, due to its excellent mechanical strength, thermal stability, and compatibility with microfabrication techniques. It enables disease-specific, reliable microfluidics and device production, making it widely preferred in advanced research and diagnostics.

- Glass- The segment accounted for 30% of the total market share, due to its excellent chemical resistance, optical clarity, and biocompatibility, making it ideal for precise analytical applications and widely used in diagnostics and laboratory research.

- Polymer- The segment accounted for 28% of the total market share. Due to its low-cost flexibility and ease of mass production, its suitability for disposable devices and rapid prototyping drives widespread use in diagnostics and research.

- PDMS- The segment accounted for 20% of the total market share, due to its flexibility, transparency, and ease of fabrication. Its biocompatibility and suitability prototyping make it widely used in research and microfluidic device development.

Europe Microfluidics Market Share, By Application, 2025 (%)

| Segments | Shares (%) |

| Medical | 70% |

| Non-Medical | 30% |

-

Medical- The segment dominated the market with a 70% share, due to rising demand for rapid diagnostics, point-of-care testing, and personalized treatments, increased healthcare spending, and widespread use of microfluidics index detection to boost its strong market share.

- Non-Medical- The segment accounted for 30% of the total market share, due to applications in environmental monitoring and chemical analysis. In industrial processing, the growing demand for precise, cost-effective analytical tools supports its steady adaptation across various sectors.

Top Companies in the Europe Microfluidics Market

- Illumina, Inc.

- F. Hoffmann-La Roche Ltd.

- Revvity

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Danaher

- Merck KGaA

- Abbott

- Thermo Fisher Scientific

- Standard BioTools

Segments Covered in the Report

By Product

- Microfluidic-based Devices

- Microfluidic Components

- Chips

- Micro-pumps

- Sensors

- Others

By Technology

- Lab-on-a-chip

- Organ-on-a-chip

- Continuous flow microfluidics

- Optofluidics and microfluidics

- Acoustofluidics and microfluidics

- Electrophoresis and microfluidics

By Material Type

- Silicon

- Glass

- Polymer

- PDMS

- Others

By Application

- Medical

- Pharmaceuticals

- Medical Devices

- In-vitro Diagnostics

- Others

- Non-medical

| Material Type | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Silicon | 2.54 | 2.81 | 3.11 | 3.43 | 3.80 | 4.20 | 4.64 | 5.12 | 5.66 | 6.25 | 6.91 |

| Glass | 2.16 | 2.39 | 2.63 | 2.91 | 3.21 | 3.54 | 3.90 | 4.30 | 4.75 | 5.23 | 5.77 |

| Polymer | 3.40 | 3.83 | 4.32 | 4.87 | 5.49 | 6.19 | 6.98 | 7.86 | 8.86 | 9.98 | 11.25 |

| PDMS | 2.86 | 3.22 | 3.63 | 4.08 | 4.59 | 5.16 | 5.81 | 6.53 | 7.35 | 8.26 | 9.29 |

| Others | 0.91 | 1.01 | 1.11 | 1.22 | 1.35 | 1.48 | 1.63 | 1.79 | 1.97 | 2.17 | 2.39 |

| Application | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Medical | 8.14 | 9.11 | 10.19 | 11.41 | 12.77 | 14.29 | 16.00 | 17.90 | 20.04 | 22.43 | 25.10 |

| Pharmaceuticals | 2.17 | 2.41 | 2.68 | 2.97 | 3.30 | 3.66 | 4.06 | 4.51 | 5.00 | 5.55 | 6.16 |

| Medical Devices | 2.70 | 3.02 | 3.39 | 3.80 | 4.26 | 4.77 | 5.35 | 5.99 | 6.72 | 7.53 | 8.44 |

| In-vitro Diagnostics | 2.33 | 2.63 | 2.96 | 3.34 | 3.76 | 4.24 | 4.77 | 5.38 | 6.06 | 6.83 | 7.69 |

| Others (Medical) | 0.94 | 1.03 | 1.14 | 1.25 | 1.38 | 1.52 | 1.68 | 1.84 | 2.03 | 2.23 | 2.46 |

| Non-medical | 3.74 | 4.22 | 4.75 | 5.35 | 6.03 | 6.79 | 7.64 | 8.61 | 9.69 | 10.91 | 12.28 |

Research Methodology

Related Databooks

March 2026

March 2026

March 2026

March 2026

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Download Databook

Download Databook

Schedule a Meeting

Schedule a Meeting