North America Thermal Interface Materials Market Size, Share and Trends 2026 to 2035

North America Thermal Interface Materials Market (By Product: Elastomeric Pads, Tapes & Films, Greases & Adhesives, Metal Based, Phase Change Materials, and Others; By Application: Computer, Telecom, Medical Devices, Consumer Durables, Industry Machinery, Automotive Electronics, and Others) Industry Size, Share, Growth, Trends 2025-2035

Get a Sample

Get a Sample

Table Of Content

Table Of Content

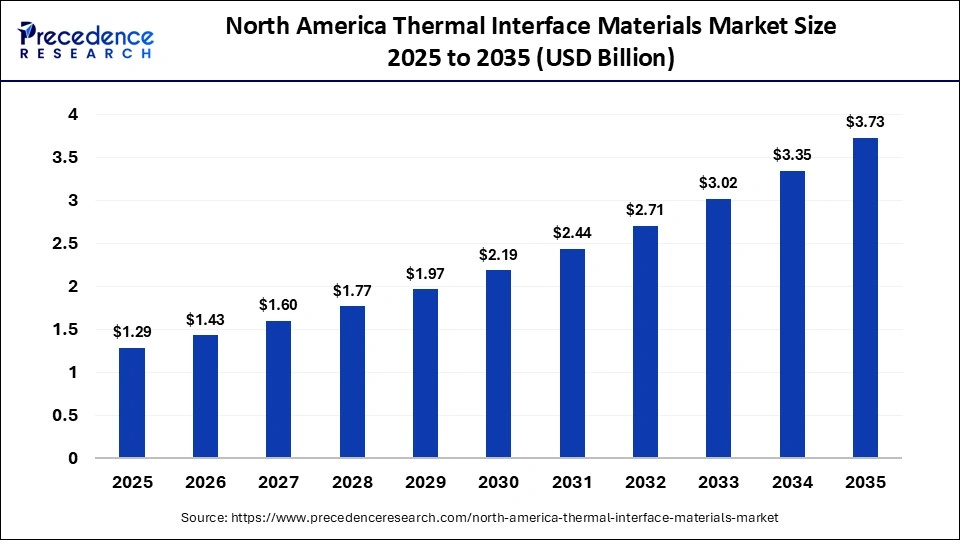

The North America thermal interface materials market size surpassed USD 1.29 billion in 2025 and is predicted to reach around USD 3.73 billion by 2035, registering a CAGR of 11.20% from 2026 to 2035. The Market is mainly fueled by the rising need for high-performance electronics, cloud and AI data centers, and electric vehicles (EVs).

North America Thermal Interface Materials Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 1.29 Billion |

| Market Size in 2026 | USD 1.43 Billion |

| Market Size by 2035 | USD 3.73 Billion |

| CAGR 2026 to 2035 | 11.20% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

Thermal Interface Materials (TIMs) play a vital role in North America's fast-growing technology and automotive industries. They replace insulating air between heated electronic parts and heat sinks to avoid overheating. This is essential for maintaining high-performance computing in large data centers, improving electric vehicle (EV) power modules, and helping the region's advanced semiconductor production. Large data centers are experiencing increasing cooling needs. TIMs such as advanced greases, gels, and adhesives are crucial for enhancing thermal conductivity and preventing hardware failures during intense AI and multi-GPU tasks.

The expansion of EVs also demands highly dependable thermal management solutions to connect battery cells with cooling plates, ensuring durability and safety. The deployment of 5G and IoT networks needs strong infrastructure that heavily depends on efficient heat dissipation for both consumer and industrial electronics. Key material choices differ by application, including traditional thermal greases and pastes, solid pads, gels, and phase change materials. Major suppliers in the industry within the region include Dow Inc., Honeywell International Inc., and Henkel.

North America Thermal Interface Materials Market, By Product, 2025

| Segments | Shares (%) |

| Elastomeric Pads | 24.80% |

| Tapes & Films | 13.90% |

| Greases & Adhesives | 27.30% |

| Metal Based | 11.80% |

| Phase Change Materials | 15.10% |

| Others | 7.10% |

- Elastomeric Pads - The elastomeric pads, with a share of 24.80% in 2025, also known as gap filler pads, are essential in the North America Thermal Interface Materials (TIM) market as they provide a clean, mess-free, and easy-to-assemble option compared to traditional thermal greases. They ensure consistent gap-filling, electrical insulation, and vibration dampening, which helps protect heat-sensitive electronics during mass production.

- Tapes & Films - The Tapes & Films segment, with a share of 13 .90% in 2025, plays a crucial role in the North American Thermal Interface Materials (TIM) market, particularly for cooling and safeguarding high-density, miniaturized electronics. Tapes and films are favored for their simple application, lightweight nature, and better mechanical compliance than traditional pastes or greases.

- Greases & Adhesives - The greases and adhesives segment, with a share of 27.30% in 2025, serves as a key foundation of the North American Thermal Interface Materials Market (TIM), holding the largest market revenue share among product types. These materials are highly regarded for their excellent gap-filling ability, thermal conductivity, and capacity to maintain minimal bondline thicknesses.

North America Thermal Interface Materials Market, By Application, 2025

| Segments | Shares (%) |

| Computer | 22.60% |

| Telecom | 14.30% |

| Medical Devices | 10.70% |

| Consumer Durables | 16.40% |

| Industry Machinery | 13.20% |

| Automotive Electronics | 17.50% |

| Others | 5.30% |

- Computer - The computer segment, with a share of 22.60% in 2025, is a fundamental and leading segment of the North American Thermal Interface Materials (TIMs) market due to the region's extensive data center infrastructure and high-performance computing (HPC) requirements. The rapid evolution of microprocessors requires materials like thermal greases, pads, and phase-change materials to fill tiny gaps and dissipate substantial heat, ensuring optimal performance and preventing hardware failures.

- Telecom - In North America, the telecom segment, with a share of 14.30% in 2025, is crucial to the Thermal Interface Materials (TIMs) market, driven by the swift deployment of 5G infrastructure and the increasing demand for high-speed connected devices. As networks upgrade, telecom infrastructure produces much more heat, needing advanced materials such as gap fillers, thermal pads, and engineered greases to maintain equipment reliability.

- Medical Devices - The medical device sector, with a share of 10.70% in 2025, plays a vital role in the North America Thermal Interface Materials (TIM) market due to high demand for dependable temperature control in diagnostic equipment and wearables. Proper thermal management is crucial to avoid overheating of sensitive electronic components, ensuring life-saving reliability and compliance with regulatory standards.

Competitive Landscape

The North America Thermal Interface Materials (TIM) market is very consolidated and led by major global tech and material science companies. Key players enhance their market share through significant R&D spending, mergers, and strategic partnerships to cater to fast-growing sectors such as electric vehicles (EVs), aerospace, and AI/cloud data centers.

- 3M Company is a prominent US manufacturer that offers a wide range of TIMs, including thermally conductive acrylic interface pads, epoxy adhesives, and tapes that are widely used in consumer electronics and automotive sectors.

- Henkel AG & Co. KGaA leads both the global and North American markets with its famous Bergquist and LOCTITE brands. Their products include phase-change materials, gap fillers, and liquid adhesives designed for high-reliability EV batteries and telecom infrastructure.

- Dow Inc. provides silicone-based reworkable gap fillers, thermally conductive compounds, and gels. They have recently teamed up with Carbice to incorporate aligned carbon nanotube technology into their semiconductor and high-performance mobility products.

- Honeywell International Inc. is a market leader with a strong presence in data centers, telecom, automotive, and industrial sectors. They focus heavily on innovative phase change materials (PCMs) and specialized thermal grease.

- Momentive Performance Materials is an emerging leader that concentrates on customer-specific, high-performance thermal solutions, particularly silicone-based gels and compounds for electronics and automotive uses.

- Parker Hannifin Corporation (Chomerics) offers a broad array of EMI shielding and thermal management solutions, including dispensable thermal greases, thermally conductive insulators, and graphite-based materials.

- Indium Corporation specializes in metal-based TIMs, liquid metal thermal interface materials (like gallium alloys), and solder materials that are essential for high-power semiconductor packaging and aerospace.

Segments Covered in the Report

By Product

- Elastomeric Pads

- Tapes & Films

- Greases & Adhesives

- Metal Based

- Phase Change Materials

- Others

By Application

- Computer

- Telecom

- Medical Devices

- Consumer Durables

- Industry Machinery

- Automotive Electronics

- Others

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at sales@precedenceresearch.com

Frequently Asked Questions

Ask For Sample

No cookie-cutter, only authentic analysis – take the 1st step to become a Precedence Research client

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Schedule a Meeting

Schedule a Meeting