U.S. Electroplating Market Size, Share and Trends 2026 to 2035

U.S. Electroplating Market (By Type: Barrel Plating, Rack Plating, Continuous Plating, and Line Plating; By Metal Type: Gold, Zinc, Platinum, Copper, Nickel, Chromium, and Others; By End Use: Automotive, Electrical & Electronics, Aerospace & Defense, Jewelry, Industrial Machinery, and Others) Industry Size, Share, Growth, Trends 2025-2035

Get a Sample

Get a Sample

Table Of Content

Table Of Content

U.S. Electroplating Market Size and Forecast 2026 to 2035

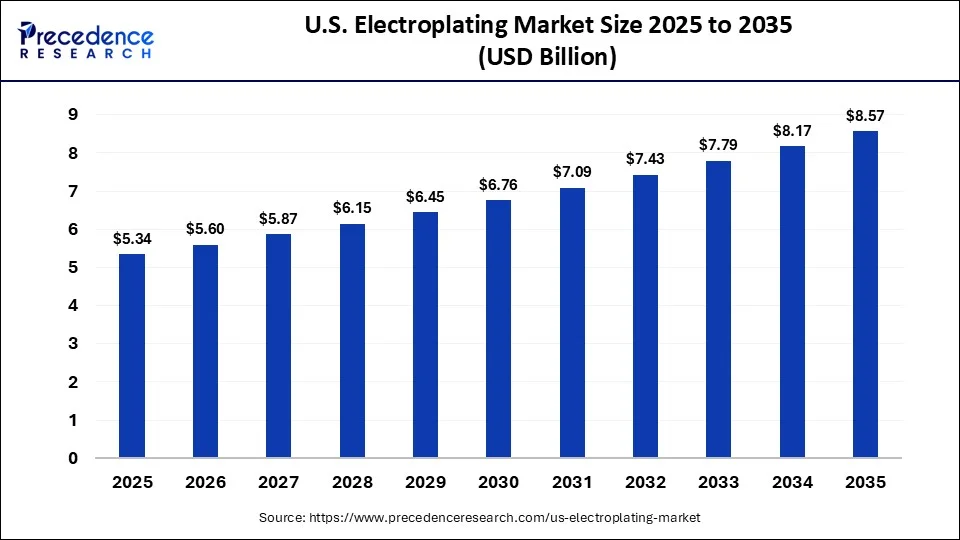

The U.S. electroplating market size is calculated at USD 5.34 Billion in 2025 and is predicted to attain around USD 8.57 Billion by 2035, expanding at a CAGR of 4.84% from 2026 to 2035. The market is mainly driven by the automotive sector, electronics, and aerospace manufacturing for the increasing need for durable, corrosion-resistant parts, and the use of eco-friendly plating agents to comply with strict environmental regulations.

U.S. Electroplating Market Statical Scope

| Reports Attributes | Statistics |

| Market Size in 2025 | USD 5.34 Billion |

| Market Size in 2026 | USD 5.6 Billion |

| Market Size by 2035 | USD 8.57 Billion |

| CAGR 2026 to 2035 | 4.84% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

The U.S. electroplating market is a crucial part of American manufacturing. It offers essential surface treatments such as corrosion resistance, wear protection, and conductivity for important components in the automotive, electronics, aerospace, and medical device sectors. This process is vital for downstream manufacturing. Plating is necessary for creating printed circuit boards (PCBs), semiconductors, EV battery terminals, and aerospace engines. Electroplating significantly increases the lifespan of metals by shielding them from environmental factors, UV light, and chemical exposure.

The industry is adjusting to strict U.S. EPA and environmental regulations by moving towards eco-friendly plating methods and safer chemical options. Automation, real-time detection of chemical degradation, and AI-driven process optimization are being used to minimize waste and enhance compliance. The transition to electric vehicles (EVs) and renewable energy is creating a specific demand for lightweight materials and conductive battery components.

U.S. Electroplating Market, By Type, 2025

| Segments | Shares (%) |

| Barrel Plating | 24.80% |

| Rack Plating | 33.70% |

| Continuous Plating | 22.10% |

| Line Plating | 19.40% |

- Barrel Plating - The barrel plating segment, with a share of 24.80% in 2025, plays a crucial role in U.S. electroplating as it is the most affordable and efficient way to mass-produce millions of small metal parts. It supports the American automotive, aerospace, hardware, and electronics sectors, enabling high-volume production.

- Rack Plating - The rack plating segment, with a share of 33.70% in 2025, is dominating the U.S. electroplating industry as it handles large, complex, or delicate parts. It is necessary for the precise, defect-free coatings needed in high-value sectors like automotive, aerospace, defense, and medical devices, where both structural integrity and appearance are critical.

- Continuous Plating - The continuous plating segment, with a share of 22.10% in 2025, is vital to the U.S. electroplating industry as it allows for automated, high-volume production of electronic and automotive components. It guarantees uniform coating and high precision, making it essential for mass-producing important technology. This segment is also key for the high-speed, uniform coating of long materials such as wires, tubes, and thin metal strips.

U.S. Electroplating Market, By Metal Type, 2025

| Segments | Shares (%) |

| Gold | 11.80% |

| Zinc | 22.70% |

| Platinum | 5.60% |

| Copper | 18.90% |

| Nickel | 20.40% |

| Chromium | 13.20% |

| Others | 7.40% |

- Gold - The gold segment, with a share of 11.80% in 2025, is a fundamental part of the U.S. electroplating industry due to gold's unique scientific properties. Its ability to ensure stable electrical conductivity, corrosion resistance, and biocompatibility makes it indispensable in high-tech manufacturing, aerospace, and medical fields.

- Zinc - The zinc segment, with a share of 22.70% in 2025, is leading U.S. electroplating as it provides a cost-effective, sacrificial corrosion protection for steel and iron substrates. By corroding preferentially, zinc protects the underlying metal, significantly prolonging the life of components across major American industries like automotive, aerospace, and construction.

U.S. Electroplating Market, By End Use, 2025

| Segments | Shares (%) |

| Automotive | 31.20% |

| Electrical & Electronics | 24.60% |

| Aerospace & Defense | 13.80% |

| Jewelry | 8.70% |

| Industrial Machinery | 15.10% |

| Others | 6.60% |

- Automotive - The automotive sector, with a share of 31.20% in 2025, is dominating the U.S. electroplating industry. It fuels significant market growth by guaranteeing vehicle safety, protecting against corrosion in tough conditions, and meeting consumer aesthetic preferences. This sector creates a high demand for durable, corrosion-resistant, and visually appealing metal parts that comply with strict safety and durability standards.

- Electrical & Electronics - The Electrical and Electronics (E&E) sector, with a share of 24.60% in 2025, is one of the most important contributors to the U.S. electroplating industry. This sector is crucial as electroplating delivers the necessary electrical conductivity, corrosion resistance, and solderability for sensitive, advanced components such as semiconductors and circuit boards.

Competitive Landscape

The U.S. electroplating market is very competitive and consolidated, focusing on sustainability, efficiency, and advancements in electronics and automotive sectors. Both major industry players and smaller specialized shops work together to offer chemical solutions, equipment, and finishing services. The industry is quickly moving towards eco-friendly technologies, automated plating lines, and strict environmental compliance.

- DuPont is a major global player providing advanced chemical formulations, including specialized materials and semiconductor metallization technologies.

- MacDermid Enthone Industrial Solutions offers specialized chemicals and surface treatments, particularly for industrial, electronic, and automotive uses.

- Coventya, now part of Enthone/MacDermid, is recognized for its eco-friendly electroplating solutions and strong technical support.

- Technic Inc. is a leading U.S. company that supplies specialty chemicals, advanced electroplating equipment, and analytical controls.

- Pioneer Metal Finishing is one of the largest specialized metal finishing companies in the U.S., providing a wide range of anodizing, hard coating, and plating services across various industries.

- Sharretts Plating Co. (SPC) is a well-known U.S. plating service company that specializes in custom metal finishing, electroforming, and engineering coatings.

- Lincoln Industries is noted for its high-end metal finishing processes, including decorative and functional chrome and nickel plating.

Segments Covered in the Report

By Type

- Barrel Plating

- Rack Plating

- Continuous Plating

- Line Plating

By Metal Type

- Gold

- Zinc

- Platinum

- Copper

- Nickel

- Chromium

- Others

By End Use

- Automotive

- Electrical & Electronics

- Aerospace & Defense

- Jewelry

- Industrial Machinery

- Others

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at sales@precedenceresearch.com

Frequently Asked Questions

Ask For Sample

No cookie-cutter, only authentic analysis – take the 1st step to become a Precedence Research client

sales@precedenceresearch.com

sales@precedenceresearch.com

+1 804-441-9344

+1 804-441-9344

Schedule a Meeting

Schedule a Meeting